BRICS+ könnte zu einem wichtigen globalen Akteur im Bereich Mineralien werden, doch interne Rivalitäten und eine schwache Regierungsführung schränken seine Fähigkeit zur effektiven Koordinierung ein.

Since its founding in 2009, BRICS has centred its cooperation on economic and trade relations. Originally initiated by Russia, the group, comprising Brazil, Russia, India and China (BRIC), was established to unite emerging economies and boost trade among its founding members. Following the addition of South Africa in 2010, which extended its representation to the African continent, the organisation officially became BRICS.

In August 2023, under South Africa’s presidency, around 40 countries signalled their interest in becoming members of BRICS. This led to the invitation of six new members – Argentina, Egypt, Ethiopia, Iran, Saudi Arabia and the United Arab Emirates (UAE) – whose membership officially began in January 2024, at which point BRICS became known as BRICS+ (BRICS Plus). These countries were reportedly selected based on their existing economic ties, energy resources and shared interest in financial coordination, particularly in advancing de-dollarisation efforts. The list was notable for the disproportionate emphasis given to the Middle East and Africa due to geopolitical, economic and strategic reasons.

BRICS’ 2024 expansion also brought in several countries with world-leading oil reserves and significant influence in global energy markets. The inclusion of the UAE has strengthened the group’s energy profile, with BRICS+ now accounting for 43.1% of global oil production, 44% of oil reserves, 35.5% of global gas production and 53% of gas reserves. Excluding Argentina, which had had an election and change in foreign policy outlook in December 2023, BRICS+ came to represent some 45% of the world’s population and 35% of global GDP (by purchasing power parity). Following the Russia-hosted 2024 BRICS+ summit, the group also announced nine partner countries.

Yet the BRICS+ group – as all international groups – is only as strong as the force of its consensus. It therefore has numerous weaknesses and strengths. Among the weaknesses is the fact that the group has no formal treaty establishing obligations and conditions. It also has to navigate regular geopolitical competition among its members, particularly China and India, Iran and Saudi Arabia, and now Egypt and Ethiopia. The association’s strengths include shared ideas which, for the most part, have developed and guided the association for over sixteen years. These include mutual development, multilateralism, global governance reform and solidarity – themes that have featured in every post-summit communique.

Since BRICS’ creation, its member countries have been confronted with the challenge of stepping up their cooperation in different economic sectors. The surging demand for raw materials is also testing them, as is the emergence of new frontiers marked by decarbonising economies. Per the World Trade Organisation’s (WTO’s) data, global trade in critical minerals has grown by an average of 10% per year over the past two decades. Between 2017 and 2022, the total value of worldwide imports has nearly doubled, rising from USD 212 billion to USD 378 billion. The main areas of growth are in platinum group metals (PGMs), such as rhodium, iridium, ruthenium and osmium, with these growing by an annual rate of 72%. Helium and lithium have also recorded exceptional growth, at 53%. China is both the largest importer of critical minerals and among the highest exporters, representing some 33% of the world's total. Behind China is the EU, representing 16%.

The growing interest in critical raw materials (CRMs) also presents an incentive for cooperation through the promise of equitable development and a stake in shaping global environmental policy. Critical minerals are essential for green and digital transitions. To date, however, there has been limited tangible cooperation among BRICS members in the mineral sector, despite repeated calls for enhanced economic collaboration in recent declarations.

Against this backdrop, we ask: How can African members of BRICS+ adapt and strengthen their position in metal and mineral markets as the group expands, and what contributions can the newly joined members offer to the European Union (EU) in this area? This paper focuses on African BRICS members, notably South Africa, Egypt and Ethiopia, and how their evolving roles within the group could shape relations with the EU. Methodologically, we draw from a range of official policy documents produced by the BRICS+ governments, the African Union (AU) and the EU as well as peer-reviewed literature with a focus on the 2015-2025 timeframe. Trade data is sourced from the WTO.

The expansion of BRICS into BRICS+ has brought new energy to the group and could reshape cooperation in the minerals sector. As minerals become critical to the low-carbon and digital transitions, BRICS+ countries now hold a commanding position in global production and reserves. They are both using geopolitical competition for access to minerals and metals to reshape their national policies and redefine their roles in mineral supply chains.

Together, BRICS+ controls 72% of the world's rare earths (and counts three of the five countries with the largest reserves among its members), 75% of the world’s manganese, 50% of the world’s graphite, 28% of the world’s nickel and 10% of the world’s copper (excluding Iran’s reserves). China leads global production of rare earth elements (REEs) with 40%, followed by Brazil (19%), Russia (9%) and India (6.2%). This dominance gives the bloc a unique opportunity to build on its resource base and step up its role in shaping global supply chains. This could be achieved through increased beneficiation, including by positioning refinement closer to where resources are mined, provided the geopolitical barriers and internal stumbling blocks can be overcome.

Each BRICS+ country is moving forward with its own strategy to secure critical mineral supplies and strengthen its place in global value chains. India set out its Critical Minerals Strategy in 2023 to reduce import dependence and attract new investment, while South Africa rolled out its Critical Minerals and Metals Strategy in 2025 to build up its processing capacity and industrial linkages. Among the new members, only Indonesia has stood out so far as a major mining nation, drawing on its nickel reserves and deepening ties with China to expand downstream processing. Others, including Egypt, Ethiopia, Iran, Saudi Arabia and the UAE, have yet to lay out clear mineral policies or tap into their subsoil potential.

Although, in their 2025 Rio Summit declaration, the BRICS+ countries set out the importance of minerals for energy security and low-emission transitions, no joint policy framework has been agreed upon. Diverging economic priorities and geopolitical alignments continue to hold back collective action. Russia and China have stepped up bilateral cooperation in mining since the Russian invasion of Ukraine in 2022. India’s participation in the US-led Minerals Security Partnership (MSP) in 2023 and growing partnerships with the EU, the US and Australia reflect its intent to balance out China’s influence. Meanwhile, the UAE is increasingly positioning itself as a competitor to China, while Brazil is diversifying its partnerships with the EU, Germany and the US. Overall, BRICS+ serves more as a flexible platform for selective cooperation than a unified bloc. Member states are likely to build on bilateral opportunities, including increased cooperation in the mineral sector with African countries, rather than push for a single coordinated minerals strategy.

Looking ahead, BRICS+ could adopt an approach similar to the MSP Forum by promoting coordinated public and private investment in critical mineral supply chains. With its strong resource base, the bloc is already well positioned to shape future market dynamics. However, concentrating exclusively on intra-BRICS cooperation would limit the flexibility of member states. In practice, countries are more likely to pursue a mix of engagement channels – bilateral, regional and multilateral – to expand their partnerships and strengthen resilience across supply chains. This diversification strategy would allow BRICS+ members to balance national priorities with the shared ambition of increasing collective influence in global mineral governance.

As of January 2024, three African countries – South Africa, Egypt and Ethiopia – have been members of BRICS. Together, they represent three of the seven largest economies on the continent. South Africa, for example, remains one of the world’s most mineral-rich nations, holding substantial reserves of PGMs, manganese, chromium, gold and coal (table 1). A coordinated effort to establish BRICS-backed processing and refining facilities in these countries could therefore help move African mineral exports further up the value chain. In addition, leveraging BRICS infrastructure financing could support the development of strategic corridors, such as railroads from the Democratic Republic of Congo to South Africa or from Ethiopia to the Suez Canal. South Africa, Egypt and Ethiopia have also developed partnerships with other BRICS+ members in the field of raw materials – for instance, South Africa with India, China, Russia and Iran, and Egypt with Saudi Arabia.

| Mineral | Africa’s global share | Major producers | Use |

| Chromium | Approximately 80% of the world's chromium reserves | South Africa, Egypt | Chromium is used in a variety of applications, including stainless steel, pigments and refractory materials. |

| Manganese | Approximately 85% of the world's manganese reserves | South Africa, Gabon | Manganese is essential for industrial applications, including the production of steel, batteries and fertilisers. |

| Platinum group metals (PGMs) | Approximately 80% of the world's PGM reserves | South Africa, Zimbabwe | Platinum, palladium and rhodium are used as catalysts in fuel cells for hydrogen-based energy systems. |

| Rare earth elements (REEs) | Approximately 15% of the world’s REEs | Egypt, Ethiopia, South Africa | Electronics, clean energy technologies and medical devices. |

Source: Boafo et al. (2024).

As the global shift toward clean energy gathers pace, the strategic importance of these resources has come to the fore. Looking ahead to its G20 presidency in 2025, South Africa has placed critical minerals high on its agenda, particularly within the task force on inclusive economic growth, employment, industrialisation and reduced inequality. Beyond the MSP Forum, the country is using the presidency as a platform to reinforce its global standing and engage a wider range of partners. This move aligns with the EU’s efforts to step up engagement with resource-rich countries amid shifting geopolitical dynamics. South Africa hosted the MSP Forum alongside the Mining Indaba 2025, signalling its leadership role and intent to leverage such platforms to foster collaboration, transparency and shared investment in critical mineral projects. South Africa also uses instruments such as its Critical Minerals and Metals Strategy and engagement in frameworks like the Clean Trade and Investment Partnership with the EU to deepen cooperation and industrial policy coordination.

In contrast, Egypt and Ethiopia – despite their significant mineral reserves – have only recently begun to take stronger steps to tap into this potential. So far, both countries have played a limited role in raw materials and regional integration, partly because critical minerals have not yet been a national priority. However, both are now focusing on creating economic incentives and implementing macroeconomic reforms to attract investment in the raw materials sector. Egypt, like South Africa, is a panel member of the United Nations (UN) Secretary-General’s Panel on Critical Energy Transition Minerals, which aims to intensify cooperation between different stakeholders in the field of critical minerals and focuses on the aspects of equity, transparency, investment, sustainability and human rights.

Within the BRICS+ bloc, the concept of criticality itself could become an important point of debate. BRICS+ members could use the forum to unpack what makes certain minerals and metals ‘critical’ – and, more importantly, for whom. The meaning of criticality varies widely across contexts, depending on a country’s mineral endowment, the role of specific resources in its industrial and economic strategies, and the perceived risks of supply disruption and price volatility. These factors, in turn, shape how each country draws up its mineral strategy and repositions itself in global value chains. Criticality is therefore not a universal label but a politically contingent concept rooted in economic and development priorities. It is poised for strategic calculations.

In the US and the EU, minerals are typically classified as critical when they are of high economic importance but scarce, leaving these economies vulnerable to import dependence, supply chain disruptions or governance risks. China, by contrast, tends to treat minerals as critical when they are abundant domestically and can be leveraged to strengthen its dominance in global markets. This approach became evident in June 2025, when Beijing restricted exports of rare earth alloys, prompting sharp reactions from the EU, Japan, the US and India.

For other BRICS+ countries, the notion of criticality is being redefined through a different lens. Indonesia, for instance, has used its vast nickel reserves to push ahead with export bans and industrial policies aimed at building domestic processing capacity – turning resource control into a tool for negotiating better positions in the global green economy. Likewise, Brazil, India and South Africa are drawing on the geopolitical competition over minerals to rethink their national policies and assert stronger roles in mineral supply chains.

BRICS+ members will use the opportunities that the alliance offers to increase bilateral and multilateral cooperation. The EU is already seen as a key source of diversification, while China – a dominant player in the global processing of critical minerals – remains for other BRICS+ members both a key partner and a competitor in the mineral value chain.

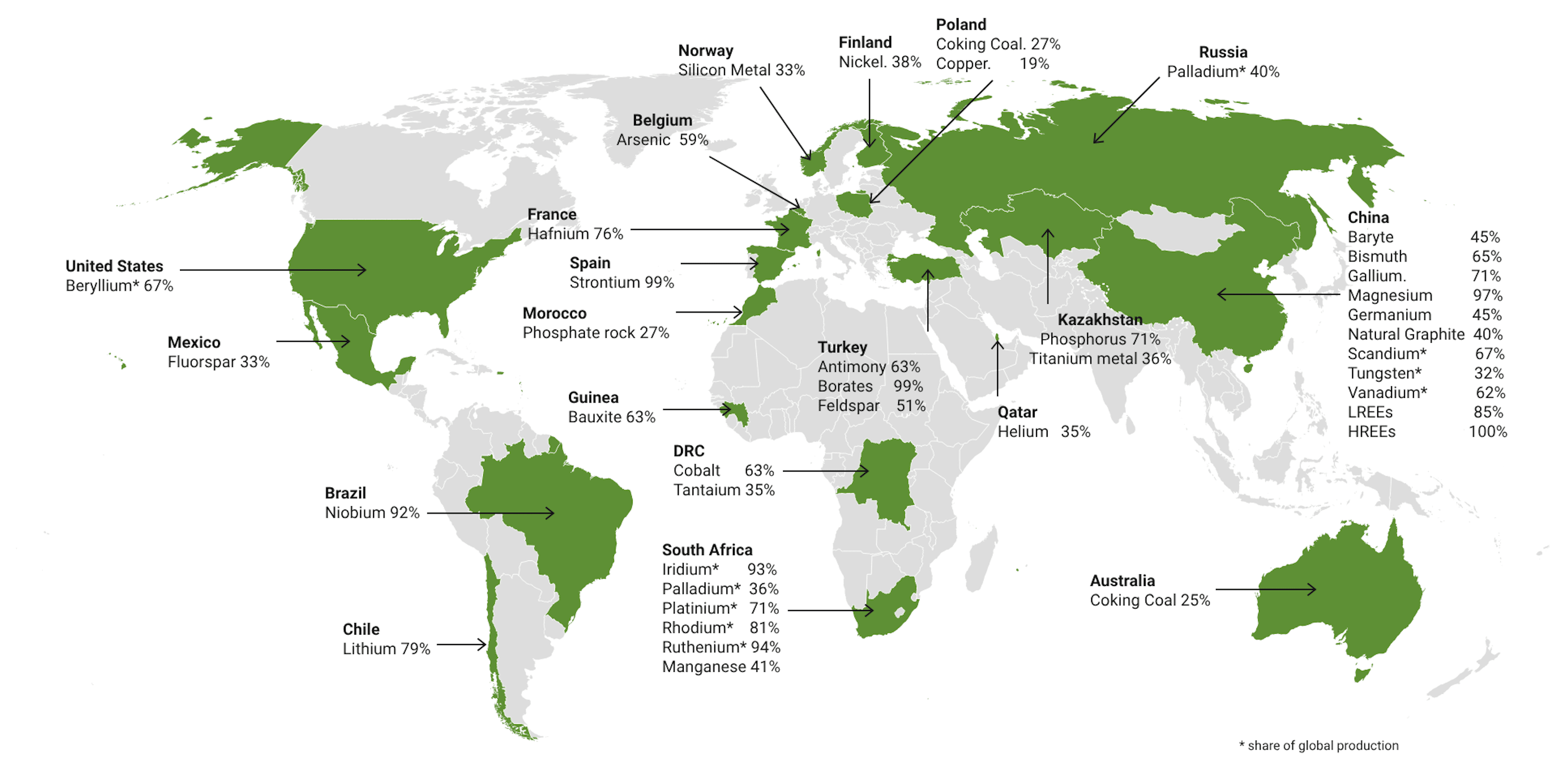

The EU also remains dependent on BRICS+ countries for certain strategic resources. For example, China provides 98% of the EU’s supply of REEs, and South Africa provides 71% of the EU’s needs for platinum and an even higher share of the PGMs iridium, rhodium and ruthenium. The EU relies on single EU companies for its supply of hafnium and strontium. Figure 1 represents the major countries in terms of their share of global exports of CRMs to the EU. CRMs are essential for a broad range of strategic sectors, including the net zero industry, the digital industry, aerospace and defence, and stand at the very beginning of each value chain.

Rather than treating BRICS+ as a single entity, the EU has generally pursued bilateral engagement with each BRICS+ country, requiring it to navigate distinct political and economic dynamics. As the EU redefines its foreign energy policies in light of recent geopolitical shifts, such as Russia’s invasion of Ukraine, there is an opportunity to move beyond emphasising divergences with BRICS+ and instead build on shared priorities to advance the energy transition. Strengthening cooperation with BRICS+ members could support mutual goals in sustainable development and resource security while managing strategic differences in a more constructive way.

During the EU-South Africa summit held in March 2025, and as part of the new EU-India strategic agenda of September 2025, CRM came up as a central topic, leading both sides to commit to stronger cooperation in the minerals sector. Given that the EU already supports South Africa’s Just Energy Transition Partnership (JETP), expanding work together on mineral extraction and processing is expected to help the country move forward on its ‘double transition’ – transforming both its raw materials and energy sectors. Highlighting the complementary interests between South Africa and the EU in critical minerals, South Africa signed, in November 2025 on the margins of the G20, a Memorandum of Understanding (MoU) with the EU to establish a strategic partnership focused on sustainable minerals and metals value chains, becoming the fifth African country to do so.

This section draws on the data and context developed in the previous parts to highlight two key considerations. Firstly, it examines how some BRICS+ members and the EU could strengthen their collaboration while constructively managing differences, and, secondly, it assesses the main strengths and weaknesses of the BRICS+ group in shaping its influence and engagement with the EU.

It is imperative to note that international cooperation among sovereign states is driven by structural and dynamic incentives. For BRICS+ members and the EU to enhance collaboration, their strategic interests should increasingly align. Three core areas require closer attention in this regard.

As Gao et al. (2024) point out, ‘although the BRICS countries have an endowment of mineral resources, they are in the low-value-added part of the global value chain, and their exports are vulnerable to price changes in the global critical metal market’. They thus have an incentive for a more stable price market. Disruptive factors include the Russia-Ukraine War, which places a limit on the potential for EU-BRICS+ cooperation. The 2025-initiated US-led global tariff escalation also has a potentially destabilising effect. As BRICS+ moves from being a source of low-value-add, the EU needs to anticipate supply disruptions from BRICS+ countries and consider alternative strategic options.

This takes us to the second element of the key strengths and weaknesses of BRICS+: cooperation. While BRICS+ and the EU are different institutional organisations, they have overlapping interests. Whereas the latter was established on the basis of a binding set of treaties, the former is still largely a loose formation made of members with divergent interests and views. BRICS+ group cooperation is further complicated by the territorial and geopolitical disputes between China and India as well as Egypt and Ethiopia. Iran and Saudi Arabia’s own relations, though on a more diplomatically stable footing since 2023, are prone to future disagreements in proxy conflicts in the Middle East. This creates challenges for both internal cohesion and external relations with potential strategic partners such as the EU.

The 2025 G20 Declaration, adopted under South Africa’s presidency, developed a mechanism that has potential for BRICS+-EU cooperation, namely the G20 Critical Minerals Framework. Although it is voluntary and non-binding, it is positioned as a “blueprint” for developing critical mineral resources into a driver of shared prosperity. Borne of the recognition of the uneven benefits from critical minerals, the Framework aims to unlock investment in mineral exploration, promote local beneficiation at source, and strengthen governance for sustainable mining practices. Further, commits to preserving what it terms “the sovereign right of mineral-endowed countries to harness their endowments for inclusive economic growth.”

Despite overlapping membership within the G20, there has yet to be a BRICS+-EU summit, or engagement at any level on any issue (let alone on CRMs). This does not preclude the potential for engagement in a less politicised mode – including through ministerial task-teams and by companies, both private and state-owned – for at least some, if not all, of the BRICS+ members. Crucially, the G20, of which both BRICS+ and the EU are members, can serve as a forum whereby consensus between the two parties can be reached and operationalised. The will is there: From the above analysis, it is evident that some of the individual BRICS+ members are open to deepening their engagement with the EU.

Based on the foregoing analysis, the prospect of a mechanism for BRICS+-EU cooperation on CRM is, at best, a decade away. Yet CRMs stand at the centre of many other issues that are at the core of the international agenda, including climate action, digital transformation, economic development and supply chain security. Importantly, one of the BRICS+ members – Russia – is considered a strategic opponent of the EU, in part due to its war on Ukraine. The most likely scenario, therefore, is one of lower-level engagement at the ministerial and company level, with some but not all BRICS+ members coming to the table.

The groundwork needs to be laid, beginning with internal BRICS+ strategic cohesion and the acknowledgement of the immediate and medium-term reality: individual BRICS+ members reaching deals with the EU, as modelled by South Africa regarding its Just Energy Transition. This begins with the recognition of the different aspirations and priorities of the individual members: African members have more urgent development needs; China and Russia have a more strategic outlook that leads to a competitive posture towards the EU. Collective BRICS+ aversion towards the CBAM presents an opportunity for the development and codification of a more inclusive approach. Inter-governmental forums such as the G20 have the potential to be a mediating space in which a broad consensus can be reached.

Boafo, J., Obodai, J., Stemn, E., & Nti Nkrumah, P. (2024). The race for critical minerals in Africa: a blessing or another resource curse? Resources Policy, 93(1).

BRICS. (2024). BRICS statement on environmental and climate-related trade measures.

European Commission. (2020, September 3). Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions.

The Kimberley Process. (n.d.). What is the Kimberley Process?

Gao, W., Zhang, H., Zhang, H., & Yang, S. (2024). The role of G7 and BRICS country risks on critical metals: evidence from time- and frequency-domain approach. Resources Policy,88, 104257.

Wilson, J. D. (2015). Resource powers? Minerals, energy and the rise of the BRICS. Third World Quarterly, 36(2), 223–239.

Bhaso Ndzendze is an Associate Professor of Politics and International Relations at the University of Johannesburg, South Africa, where he leads the 4IR and Digital Policy Research Unit (4DPRU).

Amandine Gnanguênon is Senior Fellow and Head of the Geopolitics and Geoeconomics Program. She holds a PhD in political science from the University Clermont Auvergne (France).

This policy brief is funded by the Stiftung Mercator Foundation as part of the Geopolitics and Geoeconomics of Africa-Europe Relations Project.