Nigerias riesige Gasvorkommen könnten Afrikas nächste industrielle Revolution befeuern, sofern Infrastruktur, Investitionen und politische Rahmenbedingungen so aufeinander abgestimmt werden, dass aus diesem Potenzial nachhaltige Energie entsteht.

Nigeria holds 33 percent of Africa’s gas reserves (206.5 trillion cubic feet (Tcf) proven) and is positioning natural gas as the cornerstone of its Decade of Gas (2021-2030) to drive domestic growth and regional industrialization.

A reliable gas supply is pivotal to powering Africa’s manufacturing, fertiliser, petrochemical, and steel sectors, bridging the energy access gap that leaves over 600 million Africans without electricity.

Major projects, such as Nigerian Liquefied Natural Gas (NLNG) Limited Train 7, the Ajaokuta-Kaduna-Kano (AKK) and Obiafu-Obrikom-Oben pipelines, and the Trans-Saharan/Atlantic routes, aim to boost domestic use and Liquefied Natural Gas exports to Europe and Asia.

Persistent gas flaring (188 Billion cubic feet (Bcf) in 2022), poor payment discipline in the power sector, inadequate infrastructure, and policy misalignment hinder Nigeria’s ability to fully harness its gas potential.

Reforms like the Petroleum Industry Act 2021 and Gas Flare Commercialization Programme seek to balance investment, environmental goals, and energy transition ambitions, positioning gas as a bridge fuel toward net-zero 2060.

The global energy landscape is currently undergoing a transformative shift, driven by the pressing need for sustainable energy solutions to combat climate change and address energy poverty. As countries strive to transition from fossil fuels, the imperative for sustainable industrialization becomes increasingly critical, particularly in regions like Africa where industrial underdevelopment remains a significant barrier to economic growth. Africa's industrial sector has historically lagged, hindered by inadequate energy infrastructure, limited access to reliable power, and a lack of investment in sustainable energy sources. This situation underscores the need for innovative approaches to energy supply that can support industrialization while promoting environmental sustainability.

Nigeria, endowed with the largest natural gas reserves in Africa, holding a 33 percent share as of 20241, is strategically positioned to play an essential role in driving the continent's industrial aspirations. With over 200 trillion cubic feet (Tcf) of proven gas reserves and an estimated 600 Tcf of unproven reserves,2 Nigeria has the potential to harness its natural gas resources to drive inclusive economic growth and development across the region. The Nigerian government has recognized this potential, declaring the decade from 2021 to 2030 as the ‘Decade of Gas Development’.3 This initiative aims to prioritize natural gas as crucial to the nation’s industrial growth, focusing on enhancing domestic utilization and export capabilities to meet the energy demands of neighbouring countries and regions.

This paper examines Nigeria's plans for its natural gas sector and its potential to support the industrialization of select African countries and regions. In addition to exploring the future role of gas in driving sustainable development, it also considers existing challenges such as sector underperformance, weak service delivery, and limited investment. The study analyses the feasibility of Nigeria’s ambitions and outlines the policy and institutional reforms needed to actualize them.

The significance of this research extends beyond academic inquiry; it holds substantial policy relevance for Nigerian and African policymakers, as well as industry stakeholders. By highlighting the opportunities and challenges associated with Nigeria's natural gas sector, this paper seeks to inform strategic decisions that can enhance energy security, guide energy transition, promote sustainable industrialization and ultimately contribute to the economic prosperity of the region. As Nigeria embarks on this ambitious journey, the successful development of its gas resources will not only transform its economy but also serve as a model for other African nations striving for industrial growth and sustainability.

This chapter outlines the methodology employed in this research to analyse Nigeria's natural gas sector and its potential role in facilitating sustainable industrialization across Africa. The research adopts a mixed-methods approach, combining literature review, policy review, interviews and consultations with key stakeholders. This multifaceted approach ensures a comprehensive understanding of the subject matter, allowing for a robust analysis of Nigeria's gas sector and its implications for industrial growth in the region.

The literature review encompasses a wide range of academic articles, industry reports and policy documents relevant to Nigeria's natural gas sector and the broader context of African industrialization. Key areas of focus include:

Historical context: Examination of the evolution of Nigeria's gas industry, including significant milestones and policy changes that have shaped its current state. The exploration here includes insights into the commercial exploration of petroleum and the establishment of the Nigerian Liquefied Natural Gas Limited (NLNG) in 1989, which has been pivotal in harnessing the country's natural gas resources for export and domestic use.

Status and current trends: Analysis of recent developments in the gas sector, including production levels, export capabilities, and domestic utilization. For instance, Nigeria is currently the twelfth largest producer of natural gas globally, with an annual production of approximately 3 Tcf, yet much of its potential remains underutilized due to infrastructure and regulatory challenges. The implication for the utilization of its natural gas resources in the face of a global energy transition from fossil fuels is also examined.

Comparative studies: Review of literature that compares Nigeria's gas sector with those of other African nations, highlighting successes and challenges in harnessing natural gas for industrialization. The analysis in this regard includes examining the policies and practices of countries like Algeria and Egypt, which have successfully leveraged their gas resources for economic growth.

The literature review provides foundational understanding of the existing knowledge base and identifies gaps that the research aims to address.

The policy review assesses key initiatives, regulations, and investment strategies that support Nigeria's gas sector. It covers the following issues:

Decade of gas initiative: Analysis of the Nigerian government's strategic plan for the gas sector, which aims to enhance domestic utilization and export capabilities, attract foreign direct investment, and create jobs. The initiative targets the delivery of ten major projects that are expected to significantly impact the economy, generating USD 12 billion in revenue and creating two million jobs by 2030.

Legislative frameworks: Examination of relevant legislation such as the Petroleum Industry Act and the Nigerian Energy Transition Plan, which outline the regulatory environment for gas development and utilization. The review will also consider the implications of the recent Oil and Gas Companies (Tax Incentives, Exemption, Remission, etc.) Order 2024, which aims to encourage investment in gas projects.

Critical infrastructure projects: Review of critical gas infrastructure projects, such as the Ajaokuta-Kaduna-Kano (AKK) pipeline, the Escravos-Lagos Pipeline System (ELPS), the Obiafu-Obrikom-Oben (OB3) Gas Pipeline, the Nigeria Liquefied Natural Gas (NLNG) facility, and the Floating Liquefied Natural Gas Project in Nigeria to understand their role in enhancing domestic gas utilization and supporting industrial growth.

The policy review provides insights into the institutional frameworks that underpin Nigeria's gas sector and their effectiveness in promoting sustainable industrialization.

To enrich the research findings, interviews and consultations were conducted with a range of stakeholders, including:

Policymakers: Discussions with government officials involved in energy policy and gas sector regulation to gain insights into the strategic direction and challenges facing the industry.

Industry experts: Engagement with professionals from the oil and gas sector, including operators, investors, and analysts, to gather perspectives on the operational and market dynamics of Nigeria's gas industry.

Community representatives: Consultations with local communities affected by gas projects to understand the socio-economic impacts and community engagement strategies.

These qualitative insights complement the quantitative data gathered from the literature and policy reviews, providing a well-rounded perspective on the challenges and opportunities within Nigeria's gas sector.

The data collected from the literature review, policy review and stakeholder consultations were analysed using a thematic approach. Key themes were identified to explore the relationship between Nigeria's natural gas resources and the potential for sustainable industrialization in Africa. The foci of the analysis are the following:

Feasibility of gas sector plans: Assessment of the realistic potential of Nigeria's gas sector to meet the energy needs of neighbouring African countries and support industrialization.

Current domestic commercial challenges and opportunities: Identification of barriers to effective gas utilization and strategies to overcome these challenges, including investment needs, regulatory reforms, and infrastructure development.

By employing this mixed-methods approach, the research aims to provide a comprehensive analysis of Nigeria's natural gas sector and its role in promoting sustainable industrialization across Africa. The findings contribute to the ongoing discourse on energy security, economic development and environmental sustainability in the region.

This chapter provides an overview of the existing literature on global and African energy dynamics, industrialization in Africa, and Nigeria's gas sector. The review aims to establish a comprehensive understanding of the context in which Nigeria's natural gas resources can contribute to sustainable industrialization across the continent.

The global energy landscape is currently experiencing a significant transformation, driven by the urgent need for sustainable energy solutions to combat climate change and address energy poverty. The ongoing global energy crisis, exacerbated by geopolitical tensions such as Russia's invasion of Ukraine, has led to soaring food and energy prices, further straining African economies already impacted by the COVID-19 pandemic. This crisis has resulted in an increase in the number of people living without electricity, with 4 percent more individuals lacking access in 2021 compared to 2019.4 In Africa as well, the energy landscape presents unique challenges.

In addition to infrastructure gaps and unreliable supply, Africa’s energy systems are also constrained by commercial challenges, notably the non-payment of electricity consumption costs, which undermines the financial sustainability of energy utilities and discourages private investment in grid expansion and clean energy projects. In many cases, low-income households and small businesses are either unable or unwilling to pay for electricity, often due to affordability concerns, unreliable service delivery or weak enforcement mechanisms. As a result, even where energy infrastructure exists, revenue shortfalls persist—creating a vicious cycle that hampers reinvestment and system reliability.

The challenge in Africa seems quite daunting going by the report that, ‘At present, 600 million people, or 43 percent of the total population, lack access to electricity, most of them in sub-Saharan Africa.’5 Countries such as Ghana, Kenya, and Nigeria have made significant strides in improving energy access, but substantial gaps remain. Additionally, the financial difficulties faced by utilities have heightened the risks of blackouts and energy rationing, contributing to a sharp rise in extreme poverty across sub-Saharan Africa, where the number of people affected by food crises has quadrupled in some areas. The lack of reliable and affordable energy is a major constraint on economic growth and industrialization in the region.

Despite these challenges, the global clean energy transition presents new opportunities for Africa's economic and social development. As of May 2022, countries responsible for more than 70 percent of global CO2 emissions committed to achieving net-zero emissions by mid-century, including 12 African nations that account for over 40 percent of the continent's total emissions. This shift in ambition is setting a new course for the global energy sector, particularly as clean technology costs decline and investment in renewable energy increases. In 2024, global energy investment was projected to exceed USD 3 trillion for the first time, with USD 2 trillion allocated to clean energy technologies and infrastructure. Likewise, investment in upstream oil and gas was projected to grow by 7 percent in 2024, reaching USD 570 billion, following a 9 percent increase in 2023. This growth was primarily driven by national oil companies (NOCs) in the Middle East and Asia, which have boosted their investments in the sector by more than 50 percent since 2017 and were responsible for nearly all the spending increase for 2023-2024.6

Natural gas continues to play a crucial role in the global energy mix, accounting for over 23 percent of total energy consumption, following oil (around 30 percent) and coal (around 27 percent).7 This consumption rate underscores the importance of natural gas as a transitional fuel that can help bridge the gap between fossil fuels and renewable energy sources, particularly in regions like Africa where energy demands are rising and supply gaps remain significant.

It is clear from a historical perspective that Africa's industrialization efforts have faced significant challenges. The Lagos Plan of Action (1980-2000) aimed for self-reliance but failed to achieve industrialization during the First Industrial Development Decade for Africa (IDDA I), 1980-1990, due to perennial economic crises. The Second Decade (IDDA II), 1993-2002, also fell short, lacking concrete actions and international support. The Third Decade (IDDA III), 2016-2025, proclaimed by the United Nations (UN), aims to drive inclusive and sustainable industrial development in line with the Sustainable Development Goals, particularly focusing on poverty reduction and creating resilient infrastructure.8

The December 2015 Paris Agreement, the Addis Ababa Action Agenda, the 2030 Agenda for Sustainable Development Goals (SDGs) and the African Union’s Agenda 2063 all emphasize the critical role of industrial growth in driving economic progress.9 These frameworks collectively highlight the necessity of integrating industrialization into broader strategies aimed at achieving sustainable development, particularly in the context of addressing pressing global challenges such as climate change, limited energy access and inequality.

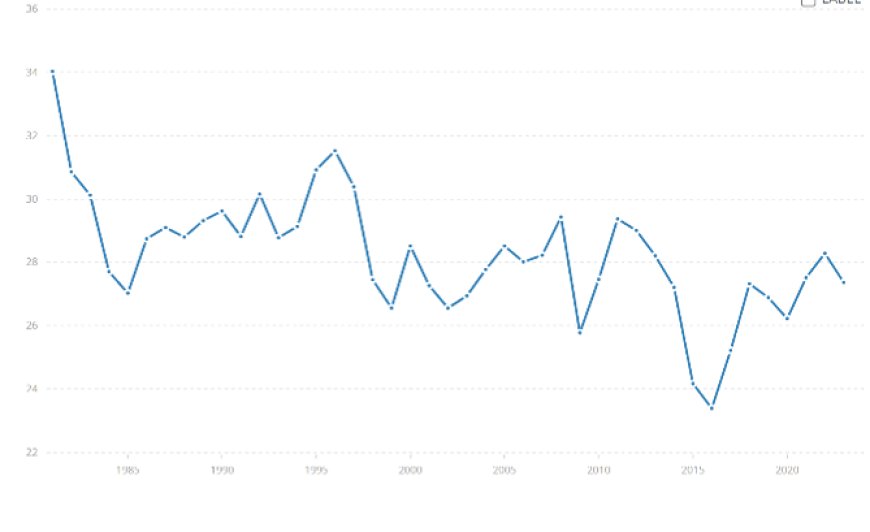

However, the industrial sector in Africa has historically lagged behind other regions, accounting for only about 10 percent of global manufacturing output.10 Political instability, inadequate infrastructure, limited access to finance and skills gaps have significantly hindered industrial development in many African countries. This situation has been further exacerbated by the COVID-19 pandemic, which has shifted the focus of African policymakers to more immediate concerns, such as surging food and energy prices driven by the conflict in Ukraine, declining global export demand, disrupted value chains and increasing external debt. Consequently, industrialization has taken a backseat amid these pressing priorities, yet it remains essential for sustained economic growth. Industry value added (percent of Gross Domestic Product (GDP)) in sub-Saharan Africa declined by 19 percent, from 34 percent in 1981 to 27.4 percent in 2023 (see Figure 2).

Despite these challenges, some African nations have made notable progress in recent years. Countries like South Africa, Morocco and Egypt have developed relatively strong manufacturing sectors, producing goods ranging from automobiles to textiles and electronics. However, the COVID-19 pandemic has had a significant impact on industrial activity in Africa, with many countries experiencing a slowdown in manufacturing output and investment.11

IDDA III is a significant global initiative aimed at advancing Africa's industrialization, closely aligned with key frameworks such as the African Union’s Agenda 2063, the African Continent Free Trade Area (AfCFTA) and the Action Plan for Accelerated Industrial Development of Africa (AIDA). With Africa's population projected to reach 2.4 billion by 2050, largely driven by a growing youth population, IDDA III seeks to leverage this demographic advantage to foster sustained economic growth through industrialization.12

A critical factor in achieving this industrial growth is the availability of reliable and affordable energy. Energy is indispensable for manufacturing, powering machinery and supporting value-added industries. As African countries work towards accelerating industrialization, ensuring access to sustainable and dependable energy sources will be vital for transforming economies and achieving rapid development.

Nigeria became an oil and gas-producing nation in 1956 following the discovery of oil in commercial quantities in present-day Oloibiri, Bayelsa State.13 However, for many years, the country's gas resources were largely underutilized, with much of the associated gas from oil production being flared.

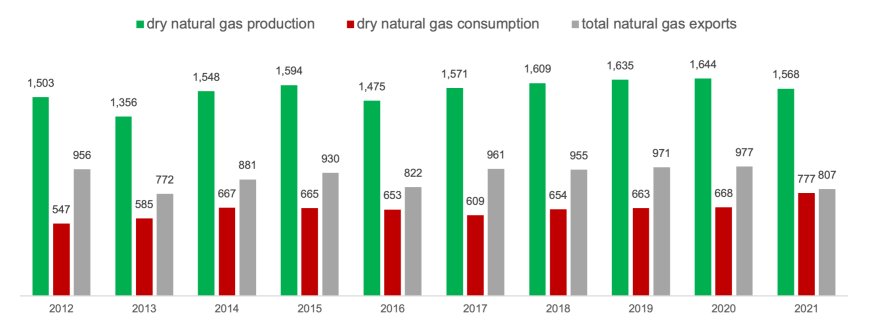

Nigeria holds significant natural gas reserves, estimated at 206.5 Tcf as of 2023, making it the eighth-largest holder of proved natural gas reserves globally.14 However, despite its vast reserves, Nigeria has struggled to effectively utilize its natural gas resources. From 2012 to 2021, dry natural gas production averaged about 1.5 Tcf annually, while domestic consumption significantly lagged behind at an average of 649 billion cubic feet (Bcf) (see Figure 3). Likewise, Nigeria exported an average of 903.31 Bcf of natural gas annually, indicating that a substantial portion of its produced gas remains unutilized. This substantial gap between production, consumption and export underscores persistent challenges in gas infrastructure, market development and access, which have limited the role of natural gas in driving national and regional industrialization.

In 2022, Nigeria ranked seventh among the world’s top LNG exporters, shipping 14.7 million metric tons, behind Australia, the U.S., Qatar, Russia, Malaysia, and Indonesia.15 Despite holding over 200 Tcf of proven and an estimated 600 Tcf of unproven gas reserves and producing about 1,554 Bcf (44 billion cubic metres (Bcm)) of natural gas in 2023,16 Nigeria remains the twelfth-largest global producer. Inadequate infrastructure and limited domestic demand are key challenges contributing immensely to the incidence of gas flaring, with 188 Bcf flared in 2022 alone —making Nigeria the ninth-highest flaring country in the world.17

The Nigerian government has outlined its intention to become a major export hub for LNG in Africa, targeting both regional markets and Asian countries such as India and China. Currently, the country operates a single LNG export terminal located on Bonny Island, which also serves as a crude oil export hub. The NLNG terminal commenced operations in 1999 and features six liquefaction trains with a combined capacity of 1.10 Tcf per year. Construction of a seventh train began in 2021 and is expected to be completed by 2026.18

Other initiatives, such as the partnership between UTM Offshore and Nigerian National Petroleum Corporation (NNPC), which will utilize feedstock from the Yoho natural gas field owned by ExxonMobil and NNPC, reflect the government’s commitment to expanding the gas sector and meeting its export goals. Between 2012 and 2021, Nigeria's domestic natural gas consumption averaged 649 Bcf per year, driven primarily by the power sector, with growing demand also observed in the commercial, residential and industrial sectors.19

To harness the full potential of its vast natural gas reserves, the Nigerian government is accelerating the development of critical pipeline infrastructure aimed at expanding domestic distribution and boosting cross-border exports. These efforts are central to Nigeria’s ‘Decade of Gas’ strategy, which positions natural gas as a key enabler of economic growth, industrialisation and regional energy trade.

One of the landmark projects in this strategy is the ELPS, operated by the Nigerian Gas Company. Originally built in 1989 with a capacity of 1.1 billion standard cubic feet per day (BSCF/D), the ELPS was significantly upgraded in 2021 with the commissioning of ELPS II—doubling its capacity to 2.2 BSCF/D.20 The pipeline transports gas from the resource-rich Niger Delta to power plants and industrial centres across southwestern Nigeria. Crucially, it also links with the West African Gas Pipeline, strengthening Nigeria’s role as a hub in the regional energy market.

Another flagship development is the Obiafu–Obrikom–Oben (OB3) Gas Pipeline, also known as the East–West Pipeline. Spanning 127 kilometres from Rivers State to Edo State, the 48-inch diameter pipeline has a capacity of 2 BSCF/D, making it one of the largest gas transmission lines in Africa.21 Operated by the Nigerian Gas Company and owned by NNPC, the OB3 pipeline is a linchpin in connecting eastern and western gas networks. It also includes an associated Gas Treatment Plant with equal throughput capacity. The OB3 project is strategically aligned with the Assa North–Ohaji South (ANOH) gas development, operated by Seplat Energy PLC. Designed to produce 300 million standard cubic feet of gas per day (300 MMSCF/D), ANOH will supply gas for the domestic market and generate approximately 2.4 gigawatts of electricity—providing a major boost to national energy access and industrial productivity.22

Together, the ELPS and OB3 pipeline systems form the backbone of Nigeria’s evolving gas infrastructure. They exemplify the country’s strategic intent to commercialize its abundant gas reserves, catalyse industrial activity, and enhance power generation—laying the groundwork for a cleaner, more resilient energy future.

Despite the challenges facing Nigeria's energy sector, the country's natural gas industry presents a promising opportunity amidst domestic priorities and global trends. In particular, the production of non-associated gas (gas extracted independently from oil), demonstrates greater resilience.23 Indeed, nearly half of Nigeria's total gas production comes from non-associated gas fields, highlighting the sector's potential for growth and development. As the global energy landscape shifts towards cleaner fuels and Africa's energy demands continue to rise, Nigeria's abundant natural gas resources offer a viable solution to meet both domestic and regional energy needs. A summary of Nigeria’s gas production and flow—including domestic use, exports, and flaring—is provided in Table 1 to clarify the distribution of gas volumes. By capitalizing on this opportunity and addressing the infrastructure and regulatory barriers that have historically hindered the sector's progress, Nigeria can unlock the full potential of its natural gas resources to drive economic growth, support industrialization and contribute to the continent's sustainable development.

|

Category |

Volume (Billion Cubic Feet - Bcf) |

Remarks |

|

Total Production |

1,500 Bcf/year (avg. 2012–2021) |

Nigeria ranked twelfth globally for natural gas production in 2022. |

|

Domestic Consumption |

649 Bcf/year (avg. 2012–2021) |

Mainly for power generation and industrial use. |

|

Export Usage |

903.31 Bcf/year (avg. 2012–2021) |

Ranked seventh among the world’s top LNG exporters. |

|

Flared/Vented/Leaked |

188 Bcf (2022) |

Ranked ninth globally for gas flaring. |

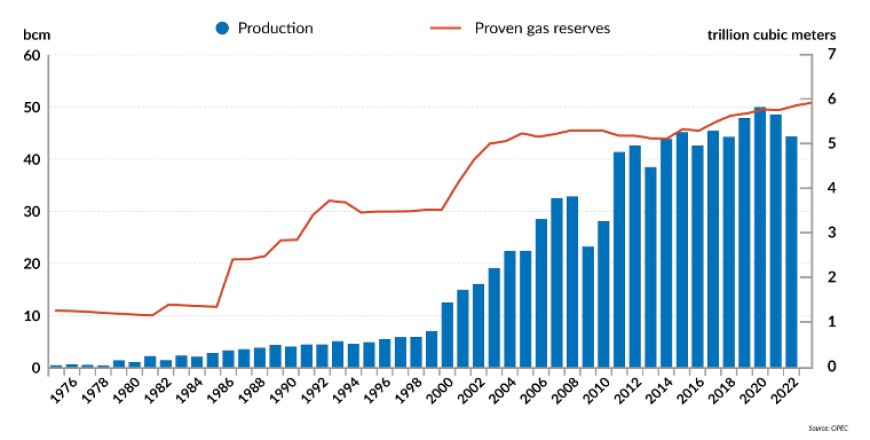

Nigeria holds the largest natural gas reserves in Africa and is the continent’s third-largest gas producer, after Algeria and Egypt. Globally, Nigeria ranks eighth in terms of proven gas reserves—behind Russia, Iran, Qatar, the United States, Turkmenistan, Saudi Arabia, and the United Arab Emirates (UAE)—yet it ranks only twelfth in production. Despite this discrepancy, Nigeria has made notable progress in increasing its gas output. Between 2000 and 2022, the country’s gas production grew by 260 percent, adding nearly 30 Bcm of gas, far outpacing Algeria’s 7 percent increase, which added just 6 Bcm over the same period.

Historically, Nigeria has struggled with high levels of gas flaring, burning off associated gas from oil production. However, from 2012 to 2022, the country reduced gas flaring by nearly 45 percent. It remains uncertain, though, whether this decline is the result of stricter regulations or the broader 40 percent drop in oil production during that time.

Successive governments have recognized the strategic importance of the gas sector, but implementation has lagged. In 2008, Nigeria launched the Gas Master Plan to become a regional gas hub by 2015, but the plan fell short of its targets. A more measured approach followed with the introduction of the National Gas Policy in 2017, reflecting the government’s continued commitment to reforming and expanding the gas industry.

The latest policy, announced in 2021, designates the 2020s as the ‘decade of gas – towards a gas-powered economy’. This ambitious plan seeks to achieve the goals set by previous initiatives and includes the development of two major gas pipelines: the Trans-Saharan Gas Pipeline,24 which would export gas from Nigeria through Algeria to Europe, and the African-Atlantic Gas Pipeline,25 an extension of the West African gas pipeline intended to transport gas to Europe via Morocco, crossing the exclusive economic zones of 13 African countries. Expanding Nigeria’s LNG export capacity is underlined as a key strategy for revitalizing growth.

The Nigerian government has implemented several plans and policies aimed at improving and harnessing its natural gas sector to drive economic growth and sustainable industrialization. Key initiatives include:

Decade of Gas Development (2021-2030): The Nigerian government has declared 2021 to 2030 as the ‘Decade of Gas Development’—a strategic initiative aimed at unlocking the full potential of Nigeria’s vast natural gas reserves, estimated at 206.5 Tcf. The programme focuses on three key objectives: expanding production, enhancing domestic utilization, and boosting export capacity. A major goal is to position Nigeria as a leading LNG exporter in Africa, with an eye on both regional markets and global demand hubs such as India and China. Equally central to this initiative is the push for domestic gas utilization. By 2030, Nigeria's domestic gas demand is projected to grow significantly, rising from about 30 percent of total gas demand in 2020 to as much as 60 percent by the end of the decade.26 This increase reflects a strategic policy shift under the ‘Decade of Gas’ initiative, which prioritizes the allocation of natural gas to critical sectors such as power generation, gas-based industries (e.g. fertilizers and petrochemicals), transportation and residential use. The drive to boost domestic utilization is aimed at reducing the country’s overreliance on oil exports, diversifying the economy and improving access to cleaner, more reliable energy sources for households and businesses. Through infrastructure investments, policy incentives and regulatory reforms—including the enforcement of Domestic Supply Obligations (DSOs)—the Decade of Gas is designed to stimulate inclusive growth and address longstanding energy poverty.

Investment in infrastructure: To support the growth of the gas sector, Nigeria is investing heavily in infrastructure development. Currently, the country operates a single LNG export terminal on Bonny Island, which has six liquefaction trains with a combined capacity of 1.10 Tcf per year. Plans are underway to construct a seventh train, expected to be completed by 2026. Additionally, the government has proposed nine more LNG terminals, with total construction investments estimated at NGN 28.3 trillion (USD 18.5 billion).

Partnerships and collaborations: The Nigerian government is actively pursuing international partnerships to expand its market base for natural gas exportation and strengthen its position in the global energy supply chain. For instance, the partnership between UTM Offshore and the NNPC aims to utilize feedstock from the Yoho natural gas field to boost production. Furthermore, the European Union (EU) has expressed its commitment to increasing LNG imports from Nigeria, recognizing the country as a reliable partner in meeting its energy needs amid the ongoing global energy crisis.27

Fiscal incentives and regulatory reforms: In February 2024, the Nigerian government introduced executive orders that provide fiscal incentives for non-associated gas projects, aiming to attract both domestic and international investment. These incentives include tax credits for qualifying projects, reduced contracting costs, and streamlined compliance with local content requirements. Such reforms are intended to create a more investor-friendly environment in the oil and gas sector, encouraging the development of natural gas resources.28 However, as with many regulatory interventions in Nigeria, the success of the Executive Orders will be dependent on their effective implementation—particularly in amending existing laws and contracts to give full legal effect to the new provisions.

Gas Flare Commercialization Programme: The Nigerian Gas Flare Commercialization Programme (NGFCP) aims to monetize flared gas and reduce environmental pollution. This programme introduces a commercial structure for the collection and use of flared gas, allowing private entities to access and utilize this resource. The NGFCP is expected to significantly reduce the volume of gas flaring in Nigeria, which was reported to be 5.32 Bcm in 2022, making Nigeria one of the highest flaring countries globally. By harnessing flared gas, the government anticipates generating substantial revenue while also addressing environmental concerns associated with gas flaring.29

Petroleum Industry Act, 2021: The Petroleum Industry Act (PIA), enacted in 2021, represents a significant reform of Nigeria's oil and gas sector, addressing longstanding challenges and establishing a more efficient regulatory framework. A key provision of the PIA is the prohibition of gas flaring and venting, as outlined in Section 105, which emphasizes the need to conserve natural resources and minimize environmental impact. This regulation aims to align Nigeria's practices with global efforts to reduce emissions. While Section 107 allows for certain exemptions, such as during facility start-ups, the overall intent is to promote responsible gas utilization and reduce waste in the industry.30

Gas Flaring, Venting and Methane Emissions Regulations, 2023: To complement the PIA, the Gas Flaring, Venting and Methane Emissions (Prevention of Waste and Pollution) Regulations, 2023 were introduced. These regulations empower the Nigerian Upstream Petroleum Regulatory Commission (NUPRC) to grant exclusive permits for accessing flared gas, thereby creating a framework for the commercialization of flared gas. The regulations set forth obligations for permit holders, including the execution of milestone agreements and gas sales connection agreements, which are essential for establishing commercial relationships and infrastructure necessary for the sale and distribution of gas.31 This regulatory framework is designed to facilitate the industrialization and commercialization of Nigeria's gas resources, contributing to economic growth.

Nigerian Energy Transition Plan: The Nigerian Energy Transition Plan outlines the government’s commitment to transitioning to a more sustainable energy system. This plan emphasizes the role of natural gas as a transitional fuel that can support the shift from more polluting energy sources to cleaner alternatives. By prioritizing natural gas development, the plan aims to enhance energy security, reduce emissions, and provide reliable energy access to the population. The integration of natural gas into the energy mix is seen as vital for powering industries, generating electricity and supporting the overall economic development of Nigeria.32

Focus on domestic consumption: The Nigerian government recognizes the importance of increasing domestic consumption of natural gas, particularly in the power sector, which is a major consumer. From 2012 to 2021, domestic natural gas consumption averaged 649 Bcf, primarily driven by the power sector.33 The government aims to enhance gas pipeline capacity to facilitate increased domestic use and support industrial growth.

Through these comprehensive plans and policies, the Nigerian government aims to harness its natural gas resources effectively, addressing energy poverty while driving sustainable industrialization. However, successful implementation will require ongoing commitment, investment in infrastructure, and alignment with broader developmental goals to ensure that Nigeria’s natural gas sector becomes a catalyst for inclusive economic growth, regional energy integration, and sustainable industrialization both domestically and across the African continent.

As of January 2024, Nigeria operates six independent LNG trains with a combined production capacity of approximately 22 million tonnes per annum (MTPA), primarily for export. These six trains are situated on a 2.27 km² plant on reclaimed land on Bonny Island along Nigeria's coastline.34 The engineering, procurement, construction, installation, testing and commissioning process for Train 7 is expected to take about four years, with an operational lifespan potentially extending 25 years or more.35 In terms of ownership, Total Energies holds a 15 percent stake in the NLNG plants, Shell has a 25.6 percent stake, and Eni owns 10.4 percent.36 Table 2 provides details on the capacity and service entry dates (ranging from 1999 to 2007) of all six LNG plants. Nigeria's LNG operations, including extraction, pipelines and plants, are primarily concentrated in the Niger Delta region.37

|

Train |

Date of entry into service |

Additional components |

Capacity (MTPA) |

Ownership |

|

1 |

February 2000 |

Gas Transmission System |

3.2 |

NLNG (NNPC, 49 percent), Shell (25.6 percent), TotalEnergies (15 percent), Eni SpA (10.4 percent). |

|

2 |

August 1999 |

3.2 |

||

|

3 |

November 2002 |

Natural Gas Liquids Handling Unit, condensate Stabilization and Liquefied Petroleum Gas production unit |

3.2 |

|

|

4 |

November 2005 |

4.1 |

||

|

5 |

February 2006 |

4.1 |

||

|

6 |

December 2007 |

4.1 |

NLNG has established long-term gas supply agreements with three joint ventures and utilizes six gas transmission systems (GTSs) to deliver gas to its complex. Of these systems, GTS-1, 2, 4, and Bonny Non-Associated Gas are located onshore, while GTS-3 and 5 are offshore. These projects maintain strong financial and export ties with Europe. There is also an increasing focus on ‘mini-LNG’ projects, such as Greenville LNG, which has been operating three LNG trains since 2019, primarily serving the domestic market.38 In addition, Axxela has reportedly secured an engineering, procurement and construction (EPC) contract for another mini-LNG project.39 Nigeria has also signed a Memorandum of Understanding for a gas export partnership involving Nigeria's Riverside LNG and Germany's Johannes Schuetze Energy Import AG. Under this agreement, Nigeria will supply 850,000 tonnes of natural gas annually to Germany, with plans to increase this to 1.2 million tonnes. The first exports are expected to begin in 2026.40

Nigeria LNG has initiated construction on a seventh train at Bonny Island, which is expected to have a capacity of 8 MTPA. Additionally, plans are underway for the development of five more trains41 A survey of media announcements and a review of the literature on ongoing LNG projects are summarized in Table 3.

|

Project |

Project developers |

Proposed capacity (MTPA) |

Status |

|

Bonny Train 742 |

NNPC, Shell, Total |

8 |

EPC awarded in 2020 |

|

Brass LNG43 |

NNPC (49 percent), ConocoPhillips (17 percent), TotalEnergies (17 percent), and Eni SpA (17 percent) |

10 |

Global Fossil Infrastructure Tracker, 2022. |

|

Nbwa Doro offshore FPSO44 |

Statoil, Shell |

5 |

Not available |

|

Olokola45 |

NNPC, Chevron Nigeria, BG, and Shell |

20 |

Presumed cancelled |

|

West Niger Delta (Western LNG)46 |

NNPC, ConocoPhillips, Chevron Texaco |

5 |

Not available |

|

Golar FLNG47 |

NNPC, Golar LNG |

Not available |

Not available |

|

Yoho Field/ UTM Offshore FLNG48 |

NNPC, UTM Offshore, Golar LNG |

Not available |

Heads of terms signed |

|

Ogbelle gas plant and Onne port49 |

Riverside LNG and Johannes Schuetze Energy Import AG |

0.85 – 1.2 |

Export partnership deal signed, project in planning phase |

Table 3 highlights the significant potential for expanding LNG capacity, which is dependent on finalizing export offtake agreements and favourable conditions in global LNG markets. Given the scale of these developments, it is crucial to evaluate the industry's past impacts and associated risks. A key development is the agreement between NNPC and the Delta State government to launch Nigeria's first Floating Liquefied Natural Gas (FLNG) project. This project is a partnership involving UTM Offshore, which holds a 72 percent equity share, NNPC with a 20 percent stake, and Delta State owning 8 percent.50 The FLNG project is expected to have a capacity of 1.8 billion tonnes per year and is valued at USD 2.1 billion.

To capitalize on this potential, the Nigerian government is working to expand its gas pipeline capacity both within the country and across borders to boost the destinations and volumes of natural gas exports. A notable project in this effort is the AKK pipeline, currently being developed by NNPC. This 614-kilometre LNG pipeline, estimated to cost USD 2.8 billion, will connect Ajaokuta to Kano. The AKK pipeline is part of the larger Trans-Nigeria Gas Pipeline (TNGP) project, which also includes a proposed pipeline linking the Qua Iboe Terminal on Nigeria's southern coast to Ajaokuta. The TNGP is a component of the broader Trans-Saharan Gas Pipeline (TSGP) project, aimed at transporting natural gas from Nigeria to Algeria through Niger, creating an alternative route for exporting natural gas to Europe via Algeria’s established international pipeline network. The development of gas infrastructure in Nigeria is set to enable the commercialization of currently flared gas and attract investments in the country's untapped gas reserves.

In addition, the Nigerian government has launched the ‘Decade of Gas Development’ initiative, which aims to prioritize natural gas as a critical engine for the nation's industrial growth. The initiative focuses on enhancing domestic utilization and export capabilities, attracting foreign direct investment and creating jobs.51 It encompasses a broad set of priorities, including the development of critical gas infrastructure (pipelines, processing facilities and virtual delivery systems), expansion of gas-for-power generation to improve electricity supply, promotion of gas-to-industry to support manufacturing and agro-industrial processing, and the rollout of gas-to-home solutions to replace biomass and kerosene for cleaner household energy.

The government is also advancing Nigeria’s position in global energy markets by scaling up gas exports through LNG and regional pipelines. A notable dimension of the strategy is the promotion of gas for transportation, using Compressed Natural Gas (CNG) and Liquefied Petroleum Gas (LPG) as cost-effective, lower-emission alternatives to petrol and diesel. The Presidential CNG Initiative and National Gas Expansion Programme (NGEP) are central to this goal, targeting widespread vehicle conversion, deployment of refuelling infrastructure, and support for local assembling of gas-powered vehicles. Underpinning these efforts are ongoing policy and regulatory reforms to attract private investment, as well as capacity-building programmes to address technical skill gaps and improve safety awareness in the gas sector. Together, these components reflect a comprehensive approach to diversifying the economy, lowering emissions, and advancing sustainable development.

Nigeria's gas sector holds significant potential to support sustainable industrialization in Africa. By leveraging its abundant natural gas resources, the country can provide reliable and affordable energy to power industrial growth across the continent. However, realizing this potential will require substantial investment in infrastructure, regulatory reforms, and effective policy frameworks.

Nigeria has been actively pursuing the development of pipelines to transport gas to Europe via the transatlantic or trans-Saharan routes, in addition to exporting LNG. These pipelines would provide Nigerian gas with access to the European market. The trans-Saharan pipeline project, a regional trade partnership involving Algeria and Niger under Economic Community of West African States (ECOWAS), is planned to be 4,128 kilometres long52 and could transport up to 30 Bcm of gas annually from Nigeria through Niger and Algeria to Europe.53 Although discussions about this pipeline began 20 years ago, recent reviews have been conducted. The estimated cost of the trans-Saharan pipeline is USD 21 billion.54 However, the project's future is uncertain following Niger’s coup in 2023, which led the new government to withdraw from ECOWAS. This has raised concerns about the pipeline’s feasibility and increased the risk that any existing infrastructure could become stranded.55

The global shift towards renewable energy to combat climate change is impacting Nigeria's oil and gas sector, as major companies reduce their investments in fossil fuels and divest from their onshore assets in the country. Shell, for example, has set a new strategy to cut total oil production by 1-2 percent annually and halt new frontier exploration investments by 2025. As a significant contributor to Nigeria’s oil and gas output, Shell is restructuring its upstream operations to fund its growth in low-carbon projects. The company is fully divesting from its onshore and shallow water assets in Nigeria, aligning with its global goal to have 55 percent gas in its portfolio by 2030. Other International Oil Companies (IOCs) like ExxonMobil and, more recently, Eni are also seeking to divest from their Nigerian onshore assets, though progress has been slowed by regulatory challenges. The Petroleum Industry Act (PIA), enacted in 2021, focuses mainly on hydrocarbons and does not extensively address the sector’s adaptation to the energy transition.

This situation raises concerns about Nigeria’s ability to attract new investments in the oil and gas sector during this global shift. Nonetheless, the Nigerian government has enacted long-term policies to support the energy transition. In 2015, Nigeria committed to reducing greenhouse gas emissions by 20 percent by 2030 compared to a business-as-usual scenario, and by 45 percent with international support. The National Renewable Energy and Energy Efficiency Policy aims to generate 30,000 megawatts (MW) of electricity from renewable sources by 2030, accounting for 30 percent of the electricity mix. The 2022 Energy Transition Plan outlines a strategy to achieve carbon neutrality by 2060, focusing on reducing emissions across power, cooking, oil and gas, transport, and industry sectors. Nigeria’s dense population, with a substantial working-age demographic, is expected to continue driving demand for telecommunications services, indicating positive prospects for the sector’s growth and, by implication, growth in the demand for clean energy to power telecommunications.

Nigeria's abundant natural gas resources present significant opportunities for regional cooperation and integration, which can drive sustainable industrialization across Africa. With the largest natural gas reserves on the continent, Nigeria is strategically positioned to leverage its resources to foster economic growth and development in neighbouring regions. However, the potential of these resources is accompanied by several challenges that must be addressed to unlock full benefits.

Underutilization of non-associated gas: Despite possessing an estimated 206.5 Tcf of natural gas reserves, Nigeria has struggled to fully exploit its non-associated gas resources. This is partly due to an unfavourable commercial environment, where weak end-user payment discipline—especially in the power sector—undermines the bankability of gas projects. The persistent inability of power generation companies (GenCos) to reliably pay for gas supplied has disincentivized investment in midstream infrastructure. Moreover, the current fiscal structure disproportionately favours upstream oil producers through the associated gas framework agreement, which allows them to offset midstream development costs against upstream tax liabilities. This creates a competitive imbalance, discouraging standalone investments in gas processing and transportation, and ultimately constraining the growth of Nigeria’s non-associated gas sector.

Deficient gas processing capability: Nigeria's gas processing capability is very deficient. The associated gas framework agreement constrains gas processing by providing fiscal advantages to upstream producers, which discourages standalone investment in midstream infrastructure. For the industry to progress, investors in gas processing facilities should be able to make investments independently and charge a toll to users of the processed gas.

Pipeline infrastructure constraints: Nigeria's pipeline infrastructure also faces constraints. The removal of subsidies in the downstream sector has unlocked the use of LPG as a cleaner alternative to kerosene, and the use of CNG has also been substantially unlocked by subsidy removal. However, the lack of sufficient pipeline infrastructure remains a barrier to the efficient distribution of natural gas across the country.

Addressing gas flaring and methane emissions: The Nigerian government has initiated a gas flare monetization programme to leverage flared gas and implement waste and prevention regulations. However, the regulation of methane abatement is not fit for purpose. Methane emissions through incomplete combustion, flaring, venting, and fugitive emissions from leaks require greater attention and more robust regulatory frameworks.

Aligning gas expansion with energy transition goals: The Nigerian Energy Transition Plan adds another layer of complexity to the development of the gas sector. Gas expansion should be aligned with the country's Nationally Determined Contribution (NDC) targets under the Paris Agreement. This requires balancing the need for gas-based industrialization with the goal of reducing greenhouse gas emissions and transitioning to cleaner energy sources

Governance and policy alignment challenges: Nigeria's gas sector faces governance challenges, with various initiatives like the Energy Transition Office, the National Council on Climate Change (NCCC), and the Decade of Gas not effectively coordinating with each other. The Energy Transition Plan sets constraints on emissions, but the Decade of Gas initiative does not fully reflect the energy transition goals. Additionally, the Nigerian government has often relied on international oil companies to drive its energy security agenda, which has negatively impacted the Petroleum Industry Act. Lack of clear understanding by key government agencies, policy misalignment, corruption, host community agitation, regulatory overlap, and limited regulatory capacity further compound these challenges.

Optimizing gas utilization metrics: To drive industrialization and economic growth, Nigeria must recalibrate its gas utilization strategy to better reflect evolving domestic and regional energy needs. Currently, a significant portion of Nigeria’s gas is allocated for export, with relatively limited supply directed toward domestic use. However, projections indicate that Nigeria’s domestic gas demand could grow from 30 percent in 2020 to as much as 60 percent by 2030.56 This anticipated increase underscores the urgent need to prioritize local and regional markets, particularly within Africa. To achieve this goal, Nigeria must make the domestic gas market more bankable and as commercially attractive as the export market—an essential but challenging prerequisite. Addressing pricing frameworks, payment discipline (especially in sectors like power) and infrastructure constraints will be critical. By rebalancing its allocation and improving the profitability of local supply, Nigeria can fuel gas-based industrialization, expand energy access, create jobs and enhance regional trade through pipelines and virtual gas networks. Such a shift would not only improve energy security at home but also strengthen Nigeria’s leadership in Africa’s emerging gas economy.

Potential impact on industrialization: Access to affordable and reliable natural gas can transform the industrial landscape in Africa. Nigerian gas can be utilized for power generation, reducing energy poverty and supporting the development of energy-intensive industries like steel, cement and fertilizers. The petrochemical industry can also benefit from Nigerian gas as a feedstock for producing plastics, chemicals and other value-added products.

Leveraging gas for industrialization: Natural gas can serve as a key driver of industrialization in Nigeria and across Africa by being processed into high-value products that support diverse industries. For instance, companies like Indorama Eleme Petrochemicals in Rivers State convert natural gas liquids—particularly ethane—into polyethylene and polypropylene used in the manufacture of plastics, packaging and textiles. Similarly, the Dangote Refinery and Petrochemical Complex in the Lekki Free Trade Zone is poised to utilize natural gas to power its massive refining and fertilizer operations, producing urea and ammonia for agricultural and industrial use. These large-scale investments demonstrate how gas-based value addition can catalyse sectoral development in manufacturing, furniture, automotive components, and consumer goods. By scaling such models, Nigeria can create substantial employment, meet regional demand and position itself as a leading hub for gas-based industrial transformation in Africa.

Infrastructure development: The development of natural gas infrastructure, including pipelines and LNG terminals, offers a platform for regional cooperation and integration. Projects like the TSGP aim to transport Nigerian gas through Niger to Algeria, connecting African countries and facilitating cross-border trade. The West African Gas Pipeline Project, a 681 kilometres pipeline, transports natural gas from Nigeria to Benin, Togo and Ghana for power plants and heat- using industries. However, the recent withdrawal of Niger from ECOWAS raises concerns about the pipeline's feasibility and the risk of stranded assets.

Beneficiary African countries and regions: West Africa and North Africa are regions that stand to benefit significantly from Nigeria's natural gas resources. Countries such as Benin, Togo, Ghana, and Morocco could utilize Nigerian gas in power generation, manufacturing and petrochemical industries. Access to reliable natural gas can help these nations address energy shortages and support their industrial growth.

Risks of stranded gas assets: As the global energy landscape shifts towards renewable energy sources, there is a risk of stranded gas assets in Africa. However, the continent's energy transition must be carefully managed to ensure that natural gas plays a complementary role in supporting industrialization and economic development. By aligning investments in gas infrastructure with long-term industrial plans and diversifying export markets, Nigeria can mitigate the risk of stranded assets and ensure the sustainability of its gas sector.

In conclusion, Nigeria's natural gas resources hold immense potential for driving sustainable industrialization across Africa. By addressing the challenges in production and leveraging the opportunities for regional cooperation and integration, Nigeria can unlock the transformative power of its gas sector in both meeting its domestic energy needs, and creating new industries and trade markets through petroleum products such as plastics industry. This approach not only benefits Nigeria but also serves as a model for other African nations striving to harness their energy resources for inclusive growth and development.

This paper presents an in-depth analysis of Nigeria's natural gas sector, its readiness to support industrialization in Africa, and the broader implications for energy supply and demand across the continent. The findings are categorized into four key areas: Nigeria's gas sector readiness, the energy demand and supply gaps in Africa, a feasibility assessment of Nigeria's gas-led industrialization plans, and the identification of policy gaps along with actionable recommendations.

Nigeria's gas sector is characterized by significant potential, but it faces several challenges that affect its readiness to support regional industrialization.

Infrastructure: As of 2024, Nigeria operates six independent LNG trains with a combined production capacity of approximately 22 MTPA. The ongoing construction of Train 7 and the development of key pipeline projects like the AKK pipeline are steps towards enhancing gas infrastructure. However, the country still grapples with inadequate infrastructure for capturing and utilizing flared gas, which remains a significant barrier to maximizing production capacity. Furthermore, the existing pipeline infrastructure is insufficient for the efficient distribution of natural gas across the country, limiting access to this critical resource.

Production capacity: Nigeria produces an average of approximately 1,500 Bcf of dry natural gas annually, based on data from 2012 to 2021. Of this volume, domestic usage averages 649 Bcf per year, primarily for power generation and industrial applications, while about 517 Bcf per year is exported as LNG, mainly via the NLNG facility. However, inefficiencies persist, as 188 Bcf of gas was flared in 2022, resulting in both economic loss and environmental harm. With proven natural gas reserves of 206.5 Tcf and current production levels around 1.5 Tcf annually, a significant gap remains between potential and actual output. This underlines the urgent need to scale up production and utilization to drive domestic value addition and regional industrialization. The government’s ‘Decade of Gas Development’ initiative aims to address these challenges through expanded infrastructure, regulatory reform and market development—but its success will hinge on effective implementation and sustained political commitment.

Regulatory framework: The Nigerian Energy Transition Plan and Petroleum Industry Act have gaps in stakeholder engagement, regulatory frameworks, environmental policies, alignment with industrial plans and financing mechanisms for the natural gas sector. The plans lack clear articulation of buy-in from civil society and the private sector, fail to sufficiently address regulatory bottlenecks hindering gas development, lack robust environmental policies prioritizing sustainable gas utilization, do not explicitly link gas projects with broader industrialization goals, and provide insufficient details on innovative financing mechanisms. Additionally, governance challenges, including policy misalignment and corruption, exacerbate these issues, hindering effective coordination among various initiatives.

The energy needs of various African regions present both challenges and opportunities for Nigeria's gas sector.

Quantifying energy needs: Despite the growth in production, Africa remains the most energy-poor continent, with nearly 600 million people, or 43 percent of the total population, having no access to electricity. Countries in West Africa, such as Ghana and Benin, and North African countries like Morocco and Egypt, face significant energy supply gaps. For instance, McKinsey estimates that African energy demand could increase by 30 percent by 2040, driven by rapid population growth and industrialization.

Bridging supply gaps with Nigerian gas: Nigeria's abundant natural gas resources can play a crucial role in addressing these energy deficits. The potential for cross-border gas trade through pipelines and LNG exports can enhance energy security in these regions. For example, the Trans-Saharan Gas Pipeline could facilitate the transportation of up to 30 Bcm of gas annually to Europe, thereby supporting regional energy demands. Moreover, optimizing gas utilization metrics to prioritize domestic consumption over exports can further enhance energy access and support industrial growth across Africa.

Assessing the realism of Nigeria's gas-led industrialization plans requires consideration of various factors:

Economic factors: The economic viability of gas-led industrialization in Nigeria is critically dependent on project bankability and the presence of credible payment guarantees. These are key determinants for attracting foreign direct investment (FDI) into the sector. Despite Nigeria’s abundant gas reserves and rising global demand—particularly from Europe due to shifting geopolitical dynamics—investors remain cautious. A history of payment defaults, especially in the power sector, combined with opaque commercial arrangements, undermines investor confidence. Additionally, overreliance on IOCs for infrastructure and energy security risks crowding out local investment and limits the development of domestic capacity. To make projects financially viable and appealing to investors, Nigeria must strengthen its financial architecture, implement transparent payment systems and de-risk projects through credible off-take agreements and government-backed guarantees.

Technical factors: The technical feasibility of expanding gas infrastructure, including pipelines and processing facilities, is critical. Nigeria must address existing challenges, such as security concerns and funding constraints, to ensure the successful execution of these projects. Additionally, the development of robust gas processing capabilities is essential for maximizing the value derived from natural gas.

Environmental factors: The global shift towards renewable energy raises questions about the long-term sustainability of gas as a transitional fuel. Nigeria's commitment to achieving net-zero emissions by 2060 necessitates careful planning to ensure that gas development aligns with environmental goals. Addressing gas flaring and methane emissions through effective regulation and implementation of the Nigerian Gas Flare Commercialisation Programme is vital for minimizing environmental impacts.

Geopolitical factors: The geopolitical landscape, particularly considering recent events in Niger, poses risks to the stability and feasibility of cross-border gas projects. Nigeria must navigate these complexities to secure its position as a regional energy hub, ensuring that gas expansion aligns with energy transition goals while fostering regional cooperation.

Identifying and addressing policy gaps is essential for realizing Nigeria's gas-led industrialization plans:

Regulatory bottlenecks: Existing regulatory frameworks may not sufficiently incentivize investment in the gas sector. Streamlining regulations and enhancing transparency can attract foreign investment and foster public-private partnerships. Additionally, aligning gas expansion with energy transition goals is crucial for sustainable development.

Infrastructure investment: While expanding gas infrastructure is critical to supporting both domestic consumption and export ambitions, these efforts must be underpinned by a viable and creditworthy domestic power sector. Nigeria’s current power sector struggles with chronic payment shortfalls and inefficiencies that deter investment. To make domestic gas utilization bankable, the government must prioritize not only infrastructure development—such as pipelines, processing plants and distribution networks—but also payment discipline and sectoral reform. Ensuring that power sector off-takers can pay fully and on time is essential to attract private capital and secure long-term supply contracts. Innovative financing mechanisms, including public-private partnerships and engagement with international development finance institutions, should be aligned with strong governance, revenue assurance and cost-reflective pricing.

Capacity building: Developing local expertise and capacity in the gas sector is crucial for sustainable growth. Training programmes and partnerships with international firms can enhance local skills and knowledge, ensuring that Nigeria can effectively manage its gas resources and infrastructure.

Environmental policies: Establishing robust environmental policies that promote sustainable gas utilization and minimize flaring is essential. Implementing the Nigerian Gas Flare Commercialisation Programme can help reduce waste and increase gas availability for domestic use, while also addressing methane emissions through comprehensive regulatory frameworks.

By addressing these challenges and leveraging the opportunities presented by its natural gas resources, Nigeria can play a pivotal role in driving sustainable industrialization across Africa, enhancing energy security and fostering economic growth.

To effectively leverage Nigeria's natural gas resources for sustainable industrialization in Africa, a comprehensive set of policy recommendations is essential. These recommendations should address the challenges identified in previous chapters while promoting investment, aligning with climate transition goals and ensuring that Nigeria's gas sector contributes to both domestic and regional development.

Streamline regulations: Simplifying and clarifying regulatory frameworks can create an environment more conducive to investment in the gas sector. This includes reducing bureaucratic hurdles and ensuring that regulations are transparent and predictable.

Align policies with climate goals: Nigeria should ensure that its gas development policies are aligned with its NDCs under the Paris Agreement. This involves integrating climate considerations into gas sector planning and investment decisions, promoting natural gas as a transitional fuel while committing to long-term emissions reduction targets.

Incentivize investment: The government should fix the power sector to ensure payment discipline and financial viability. Thereafter, it should offer targeted fiscal incentives and provide government-backed payment guarantees to de-risk private investment in gas infrastructure.

Public-private partnerships: Encouraging partnerships between the government and private investors can mobilize the necessary capital for infrastructure development. By sharing risks and rewards, these partnerships can enhance the feasibility of large-scale gas projects.

Engage international stakeholders: Nigeria should actively engage with international financial institutions and development partners to secure funding for gas infrastructure projects. Highlighting the role of natural gas in supporting energy access and industrialization can help attract investment, even in the face of increasing restrictions on fossil fuel financing.

Diversify export markets: To mitigate the risk of stranded gas assets, Nigeria should diversify its export markets beyond traditional partners. Engaging with emerging markets in Asia and Africa can provide new opportunities for gas sales and reduce dependence on specific regions.

Develop a strategic gas utilization plan: Nigeria should adopt a strategic approach to gas utilization, prioritizing domestic consumption and regional exports. By ensuring that a significant portion of gas production is directed towards local industries and power generation, Nigeria can enhance energy security while minimizing the risk of stranded assets.

Invest in clean technologies: Nigeria should invest in technologies that enhance the efficiency of gas utilization and reduce emissions, such as carbon capture and storage (CCS). This will not only improve the environmental performance of the gas sector but also align with global climate transition efforts.

Implement robust environmental regulations: Establishing stringent environmental regulations for gas flaring and methane emissions is crucial. The government should enforce compliance with these regulations to minimize environmental impacts and promote sustainable gas utilization practices.

Foster regional cooperation: Nigeria should collaborate with neighbouring countries to develop regional gas infrastructure and markets. Initiatives like the Trans-Saharan Gas Pipeline can facilitate cross-border trade, enhancing energy security and industrial growth across West and North Africa.

Develop local expertise: Investing in capacity building and training programmes for local professionals in the gas sector is essential. This can enhance local knowledge and skills, ensuring that Nigeria can effectively manage its gas resources and infrastructure.

Promote research and innovation: Encouraging research and innovation in gas technologies can lead to more efficient and sustainable practices. Collaborations with academic institutions and international research organizations can facilitate knowledge transfer and technological advancement.

This study has explored the critical role of Nigeria's natural gas sector in supporting sustainable industrialization across Africa. Despite the significant potential of Nigeria's gas resources, numerous challenges must be addressed to realize this potential fully. Through strategic policy recommendations focused on enhancing regulatory frameworks, attracting investment, addressing the risk of stranded assets, promoting sustainable development, and building local capacity, Nigeria can position itself as a key player in the energy landscape of Africa.

By aligning its gas sector development with climate transition goals, Nigeria can leverage its natural gas resources to not only meet domestic energy needs but also contribute to regional energy security and industrial growth. The successful implementation of these recommendations will require collaborative effort among government agencies, private-sector players, institutional investors, and international partners, ensuring that Nigeria's gas sector evolves into a sustainable and resilient component of the continent's industrialization strategy. Ultimately, this approach will foster economic growth, create jobs, and improve the quality of life for millions across Africa, while addressing the pressing challenges of climate change and energy poverty.

[1] Statistica. Natural gas reserves in Africa as of 2023, by main country. (2024).

[2] Uwaegbute, C., Yusuff, T., Olaniyi, B. (2021, August). The Petroleum Industry Act: Redefining the Nigerian oil and gas landscape. PricewaterhouseCoopers.

[3] Ubong, E. (2021, September 1). Industrialisation hinges on gas development, investment. Shell Nigeria.

[4] International Energy Agency. World Energy Investment 2024. (2024, June).

[5] International Energy Agency. Africa Energy Outlook 2022. (2022).

[7] Eni. Natural gas in the global energy scenario. (2023).

[8] Mwangi, C. (2020, August 11). Introduction and History of the Industrial Development Decades for Africa. Future Africa Forum.

[9] Dinh, H. (2023, October). Industrialization in Africa: Issues and Policies. Policy Center for the New South.

[11] African Development Bank. Driving Africa’s Transformation: The Reform of the Global Financial Architecture. (2024).

[12] Mwangi, C. (2020, August 11). Introduction and History of the Industrial Development Decades for Africa. Future Africa Forum.

[13] Good, L. (2022, October 20). A Brief Overview Of The Law And Development Of Gas In Nigeria. Mondaq.

[14] U.S. Energy Information Administration (EIA). (2023). Natural Gas Reserves. Retrieved from https://www.eia.gov/.

[15] Okonkwo, O. (2023, August). EU plans higher LNG exports from Nigeria between 2023 and 2027. Nairametrics.

[16] Statistica. Production volume of natural gas in Nigeria from 2013 to 2023. (2024).

[17] World Bank. Global Gas Flaring Tracker Report. (2023). Retrieved fromhttps://www.worldbank.org/.

[18] ARM. Unravelling Nigeria’s Oil and Gas Tapestry: Nigerian Oil and Gas Sector report 2024. (2024).

[20] Ojomah, N. (2024, May 2). From Policy to Pipeline: The Evolution of Nigeria's Gas Sector in the Decade of Gas. The Firma Advisory.

[21] Okonkwo, O. (2023, September 29). NNPCL, Gas and Petroleum Ministers assure of OB3 gas pipeline completion. Nairametrics.

[22] ANOH Gas Processing Plant (2024). Seplat Processing Gas.

[23] Nakhle, C. (2024, June 21). Unlocking Nigeria’s economic potential with natural gas. GIS.

[24] International Trade Administration. Algeria Trans Saharan Gas Pipeline. (2022, September 22).

[25] Morocco and Nigeria Revive Ambitious Gas Pipeline Plan Amid Energy Crunch. (2024, January 29). Pipeline Technology Journal.

[26] (n.d.). The Decade of Gas.

[27] Elliott, S. (2023, August 14). Nigeria makes new headway with floating LNG as part of gas drive. S& Global.

[28] Duru, S., Oyebode, A., Olorunmaiye, J. (2024, March 14). Reforming The Nigerian Oil And Gas Sector - The 2024 Executive Order And Directives.

[29] Odor, J. (2024). The Nigerian Gas Flare Commercialization Programme: Prospects and Challenges.

[30] Olaniwun Ajayi. (2023). An Overview of the Extant Gas Flare Regulations in the Nigerian Petroleum Industry. Retrieved fromhttps://www.olaniwunajayi.net/blog/an-overview-of-the-extant-gas-flare-regulations-in-the-nigerian-petroleum-industry/.

[32] The Firma Advisory. (2024). From Policy to Pipeline: The Evolution of Nigeria's Gas Sector in the Decade of Gas.

[34] Pepple, A., and Egba, P. (2021). Mitigating the impact of rainfall on the Bonny Island. Global Scientific Journal, 9(3), 638–663.

[35] Nigeria LNG Limited. (2019). Environmental, social and health impact assessment (ESHIA) for the Train 7 project.

[36] LNG Prime Staff. (2023, May 31). TotalEnergies renews license for Nigerian offshore block. LNG Prime.

[37] Echedu, A. J., Okafor, H. F., and Olayinka Iyiola, O. (2022). Air pollution, climate change and ecosystem health in the Niger Delta. Social Sciences, 11(11), Article 525.

[38] Global Energy Monitor. (2022). The scramble for Africa’s gas.

[39] Axxela. (2021, December). Construction of a small-scale LNG in Ajaokuta; Transit Gas and NGMC sign agreement.

[40] Onuah, F. (2023, November 21). Nigeria and Germany sign $500 mln renewable energy and gas deal. Reuters.

[41] Global Energy Monitor. (2024). NLNG – Nigeria LNG Limited.

[42] Esau, I. (2022, April 20). ‘We want project to pull through this time’: Nigeria minister talks up Brass LNG revival. Upstream Energy Explored.

[43] Global Energy Monitor. (2022). The scramble for Africa’s gas.

[44] Akintoye, A.O., Eyong, A. K., Agada, P. O, and Digha, O. N. (2016). Socio-economic implication of Nigeria Liquefied Natural Gas (NLNG) project in Bonny local government area. Journal of Geoscience and Environment Protection 4(5), 63–79.

[47] Elliot, S. (2023, August 14). Feature: Nigeria makes new headway with floating LNG as part of gas drive. S&P Global Commodity Insights.

[48] Offshore Technology. (2023, July 21). NNPC signs agreement with UTM Offshore for FLNG project.

[49] Africa Oil and Gas Report. (2023, November 22). German firm to import 1.2 MMMTPA of Nigerian LNG.

[50] African Energy Chamber. (2023). African Energy Chamber supports Nigeria’s first floating LNG development.

[51] Vazi, B., and Bridle, R. (2024, June). A Balancing Act: Considerations for the expansion of liquefied natural gas projects in Nigeria. International Institute for Sustainable Development (IISD).

[52] Rédaction Africanews. (2023, March 1). Nigerian gas, stake in an energy war in the Maghreb.

[53] Sofiullahi, A. (2024, February 14). Problems mount for Sahara gas pipeline, leaving Nigerian taxpayers at risk. Climate Home News.

[54] Holleis, J., and Schwikowski, M. (2022, April 4). Europe looks to Africa to fill natural gas gap. DW.

[55] Sofiullahi, A. (2024, February 14). Problems mount for Sahara gas pipeline, leaving Nigerian taxpayers at risk. Climate Home News.

Chibuikem Agbaegbu is a Climate & Energy Specialist with 12+ years in Sub-Saharan Africa. Expert in low-carbon electrification, energy nexus, climate transition & circular economy. Led donor/DFI projects with FCDO, USAID, EU, UNDP, GEF & more.