Nigeria’s clean energy transition is unfolding amid shifts in technology, finance, and geopolitics. This report examines China’s role in infrastructure, renewable energy, and investments shaping the sector.

Nigeria’s clean energy transition is unfolding within a larger global shift in which energy, trade, industrial policy, and geopolitical competition are becoming increasingly interconnected. This report presents Nigeria’s transition not simply as a technical move from fossil fuels to renewables, but as a strategic development question shaped by infrastructure deficits, climate commitments, industrial ambitions, and the country’s positioning among competing global partners. At the center of this analysis is China’s expanding role in Nigeria’s clean energy landscape and the strategic choices Nigeria must make to ensure that external engagement translates into domestic value creation, industrialization, and energy sovereignty.

The study begins from the reality of Nigeria’s severe energy access and infrastructure gap. Although the country has an installed generation capacity of about 13 GW, transmission constraints restrict peak generation to around 5.7 GW, against an estimated demand of 20 GW. This leaves between 86 and 110 million Nigerians without access to electricity. Against this background, Nigeria has adopted an ambitious policy architecture to drive its energy transition. The Energy Transition Plan, the 2023 Electricity Act, and the third Nationally Determined Contribution together frame a pathway toward universal electricity access by 2030, a 50 percent renewable generation share by 2030, and net-zero emissions by 2060. The report also notes that NDC 3.0, submitted in September 2025, sets emissions reduction targets of 29 percent by 2030 and 32 percent by 2035 relative to 2018 baselines, while also aiming for full electricity access and annual growth in new electricity connections. At the same time, the report highlights that Nigeria’s transition is not purely renewable-led: gas remains positioned as a transition fuel, with plans to expand gas-fired power capacity to 17 GW by 2035. This creates both opportunity and tension, especially in relation to climate finance, which is increasingly moving away from fossil fuel investments.

A major contribution of the report is its explanation of how China’s engagement in Nigeria has evolved over time. Earlier Chinese involvement centered on large-scale, policy-bank-backed infrastructure, including hydropower, gas pipelines, and transmission upgrades. The report cites projects such as the Zungeru and Mambilla hydropower plants, the Ajaokuta-Kaduna-Kano gas pipeline, flare-gas recovery pipelines, and transmission upgrades financed through China EximBank and China Development Bank. This earlier model reflected the logic of the first phase of the Belt and Road Initiative, characterized by debt-heavy, state-directed mega-projects. In contrast, the report argues that China’s current engagement is shifting under a “BRI 2.0” approach toward smaller, more commercially oriented and locally embedded projects. These newer engagements emphasize distributed renewables, supplier finance, solar and mini-grid systems, testing laboratories, local assembly, battery manufacturing, and joint ventures. The report presents this as a strategic adjustment by China in response to debt sustainability concerns, global economic pressures, and a broader policy pivot toward green development.

This shift is visible in both formal agreements and market activity. The report identifies the elevation of Nigeria-China relations to a Comprehensive Strategic Partnership in 2024 as an important anchor for bilateral clean energy cooperation. It then maps a range of specific agreements, including the 2018 renewal of the RMB-naira liquidity arrangement, Huawei’s role in off-grid solar and rural electrification, a biomass energy project in Borno State, tripartite agreements on lithium battery manufacturing with NASENI and Shenzhen LEMI, a mini-grid simulation and standardization center in Abuja, the EUR7.6 billion green hydrogen agreement with LONGi, and a USD328.8 million CMEC transmission upgrade deal under the Presidential Power Initiative. The report’s argument is that these agreements, when translated into bankable and implementable projects, can significantly accelerate Nigeria’s transition while also broadening cooperation into areas such as green hydrogen, local manufacturing, and standards infrastructure.

The study also tracks the commercial scale of China’s clean energy footprint in Nigeria. Between 2018 and 2025, Chinese clean-tech exports to Nigeria grew from about USD193 million to a peak of USD830 million in 2024, before reaching about USD762 million between January and August 2025. These exports cover grid equipment, batteries, electric vehicles, solar photovoltaics, and to a smaller extent wind technologies. The report interprets this growth as evidence of increasing alignment between Nigeria’s demand for affordable clean energy technologies and China’s capacity to supply them at scale. It also stresses that Chinese firms now dominate important parts of Nigeria’s off-grid and commercial solar markets, particularly in solar panels, inverters, batteries, solar home systems, and household or SME kits. In this sense, China is not only a project financier or infrastructure contractor; it is also deeply embedded in the technology and supply side of Nigeria’s clean energy economy.

A further strength of the study is that it does not present Nigeria’s relationship with China in isolation. Instead, it situates Chinese engagement within a broader ecosystem that includes the EU, the US, multilateral development banks, and domestic Nigerian finance actors. The study characterizes this landscape as complementary rather than strictly competitive. It notes that while the EU and US often position their initiatives as alternatives to the Belt and Road Initiative, in practice Nigeria’s energy transition is supported by multiple financing models. Chinese actors bring scale, speed, embedded supply chains, EPC capacity, and growing supplier-credit instruments. Multilateral actors such as the World Bank and African Development Bank provide concessional finance, technical assistance, guarantees, and de-risking structures. US and EU initiatives bring stronger governance, transparency, and ESG conditionalities. Nigerian institutions, meanwhile, are beginning to build a domestic architecture based on green bonds, guarantees, statutory funds, wholesale lines, and local capital mobilization. The report’s central point is that Nigeria’s pragmatic strategy is to “stack” these different capital sources and modalities in order to finance projects more effectively. A project can therefore combine concessional finance, Chinese EPC and vendor finance, and long-tenor local debt. The report sees this blended approach as more realistic and more beneficial than viewing partner engagement through a zero-sum geopolitical lens.

At the same time, the study is clear-eyed about the political economy challenges. It acknowledges that China’s role in Nigeria is associated with major opportunities: infrastructure delivery, job creation, industrialization, technology transfer, access to hard currency, and flexible financing arrangements such as naira settlement with RMB hedges. However, it also points to asymmetries in capacity and bargaining power. Chinese firms are described as having developed deep “transactional literacy” in Nigeria, with end-to-end control across supply chains, financial arrangements, logistics, and project execution. Nigeria, by contrast, is portrayed as lacking comparable institutional coordination and negotiation capacity. The report links this to fragmented state institutions, limited institutional memory, and opaque deal structures that can reduce local leverage, weaken technology transfer, and limit local content outcomes. It also highlights concerns around debt sustainability, opaque loan terms, product quality, grey-market imports, governance lapses, corruption, and policy uncertainty, including abrupt signals around import restrictions. Public perception of China, the report notes, is pragmatic rather than ideological: many Nigerians value visible infrastructure delivery and affordable products, while also expressing caution around debt, labor practices, privacy, and long-term dependence.

The geopolitical dimension of this study is equally important. Nigeria’s clean energy transition is shown to be shaped by the wider US-China trade conflict, EU climate trade instruments, and the global competition for critical minerals and clean manufacturing hubs. The report notes that tariffs on Chinese solar panels, EVs, and batteries in Western markets may push Chinese manufacturers to look more aggressively toward African markets, including Nigeria. It also explains that although Nigeria’s current exports to the EU may not be directly hit by the Carbon Border Adjustment Mechanism in major ways, CBAM still creates pressure for decarbonization and can influence industrial strategy. In this environment, Nigeria’s reserves of lithium, cobalt, nickel, and other minerals make it strategically important to both Chinese and Western actors. The report argues that balanced diplomacy gives Nigeria room to engage all sides while securing better terms on finance, industrial development, and technology transfer.

Across sectors, the study shows that Chinese engagement is broadening. In power, it spans both on-grid infrastructure and off-grid systems, with significant room for deeper participation in mini-grids, commercial and industrial solar, battery storage, testing infrastructure, and household electrification. In oil and gas, China remains important in gas pipelines, LNG-related infrastructure, and the broader gas-as-transition-fuel agenda, even as the report warns against long-term fossil lock-in. In clean cooking, Chinese involvement remains limited but potentially important in LPG distribution infrastructure, cookstove standards, and technology transfer. In transport, the report highlights growing relevance in electric mobility, especially as fuel subsidy removal and rising petrol prices make EVs increasingly significant in the mobility conversation. In industry and manufacturing, the report underscores the importance of solar assembly, battery manufacturing, mineral processing, and local value addition. It points to existing examples such as Auxano Solar’s domestic assembly capacity and NASENI’s battery partnership with LEMI, while stressing the policy challenge of balancing current demand for cheap imports with the longer-term goal of building an indigenous supply chain.

The study culminates in five strategic opportunity clusters for Nigeria-China cooperation. First is finance: deepening RMB-naira mechanisms, improving local currency settlement systems, and expanding commodity-backed or RMB-linked credit lines to relieve FX pressure and support green industrialization. Second is trade and industrialization: using China’s tariff-free policy and AfCFTA to expand value-added exports and move beyond raw commodity dependence. Third is infrastructure: scaling mini-grids, solar home systems, transmission, and utility-scale renewables, while linking new assets to regional electricity trade under WAPP. Fourth is local manufacturing and minerals: promoting Chinese-Nigerian joint ventures in solar modules, inverters, EVs, battery assembly, and refining of lithium, cobalt, and nickel. Fifth is climate diplomacy and investment: creating a Nigeria-China Energy Investment Platform under the NCIP framework to blend Chinese, Western, and domestic capital in a more transparent, country-led way.

Overall, the report’s core conclusion is that Nigeria-China clean energy cooperation should be treated as a strategic national development issue, not merely a set of isolated projects. If managed through coordinated institutions, transparent standards, measurable indicators, triangular partnerships, and strong local ownership, this cooperation can move from ad hoc deal-making to a structured platform for industrial transformation. The report, therefore, frames China not simply as an external investor but as a consequential actor in Nigeria’s attempt to build an energy-secure, industrially capable, and climate-aligned future.

Nigeria continues to face significant electricity access and reliability challenges. Although installed generation capacity is estimated at approximately 13 GW, transmission constraints limit peak generation to about 5.7 GW, while national electricity demand is estimated to be around 20 GW. As a result, a large share of the population remains without access to electricity and many connected users experience unreliable supply. These conditions have contributed to the increasing deployment of decentralized electricity solutions such as solar home systems and mini-grids.

Nigeria has adopted several policy frameworks to guide the transition of its energy sector. The Energy Transition Plan, the Electricity Act of 2023, and the country’s updated Nationally Determined Contributions outline targets that include universal electricity access by 2030, increasing the share of renewable energy in the power mix, and achieving net-zero emissions by 2060. Within these frameworks, renewable energy expansion is expected to occur alongside the continued use of natural gas as a transition fuel.

China has been involved in several major energy infrastructure projects in Nigeria over the past two decades. These include hydropower projects such as the Zungeru and Mambilla dams, transmission infrastructure upgrades, and gas pipeline projects such as the Ajaokuta–Kaduna–Kano pipeline. Many of these projects have been financed through loans from Chinese policy banks and implemented by Chinese engineering and construction firms.

More recent cooperation between Nigeria and China reflects a broader shift toward renewable energy technologies and new forms of collaboration. Partnerships now extend beyond large-scale infrastructure to include solar technologies, distributed energy systems, and technology partnerships related to renewable energy deployment. These developments correspond with broader changes in China’s overseas investment approach and Nigeria’s expanding focus on clean energy technologies.

Chinese manufacturers play a significant role in supplying equipment used in Nigeria’s renewable energy sector. Solar panels, inverters, and battery systems used in off-grid and commercial solar installations are widely sourced from Chinese companies. These technologies are used across solar home systems, mini-grid deployments, and commercial solar installations.

Nigeria’s clean energy transition involves engagement with a range of international partners. Multilateral development banks and Western development partners often provide concessional finance, guarantees, and technical support for energy projects. Chinese firms frequently participate through engineering, procurement, and construction roles as well as through equipment supply and infrastructure development. Project financing arrangements often combine different sources of finance and technical participation.

Institutional coordination plays an important role in Nigeria’s engagement with international energy partners. Differences in institutional experience and familiarity with foreign investment structures can affect project negotiation, implementation, and oversight. Strengthening institutional capacity can support more effective coordination of energy partnerships and infrastructure projects.

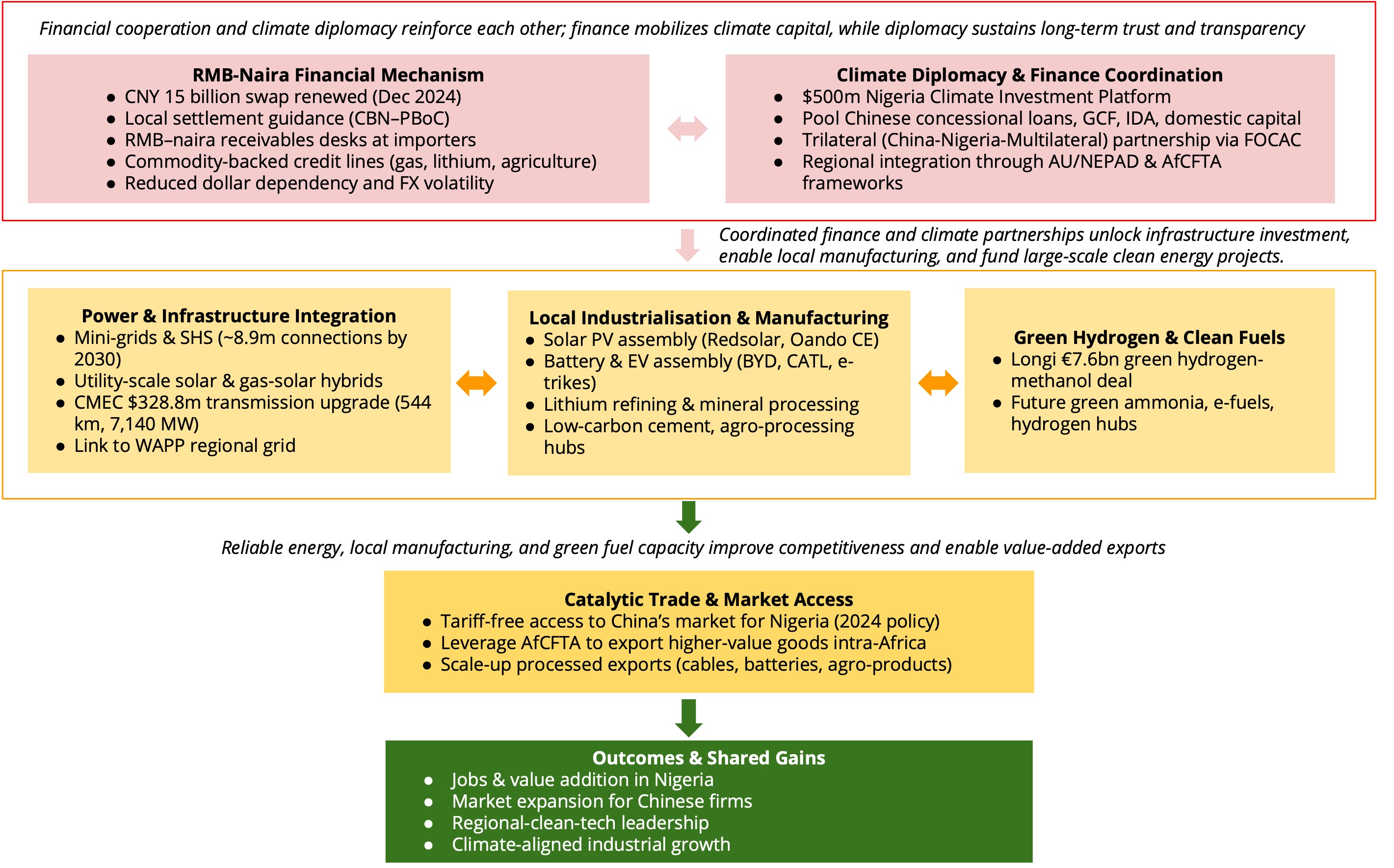

Nigeria should deepen the use of the RMB–NGN currency swap and formalize local settlement mechanisms to strengthen trade and investment ties with China. In December 2024, Nigeria renewed a Chinese yuan (CNY) 15 billion (= USD2 billion) swap agreement with the People’s Bank of China to “deepen trade ties and ease FX pressures.” To translate this into real economic impact, Nigeria could establish RMB–naira receivables desks at major importers and distributors, while the Central Bank of Nigeria (CBN) and the People’s Bank of China (PBoC) issue joint settlement guidance for cross-border transactions.

Such measures would make it easier for Nigerian importers to settle directly in local currencies, reducing dollar dependency and volatility. Additionally, commodity-backed credit lines, similar to oil-for-loan models, could be adapted to finance gas, lithium or agricultural exports that support industrial production and clean-energy value chains. This would not only expand access to liquidity for Nigerian firms but also provide China with a reliable pipeline of resource inputs for its growing green-technology sector. Overall, enhanced RMB–naira cooperation provides a financial foundation for green industrialization, anchoring predictable trade flows, easing foreign-exchange constraints and creating new channels for Chinese development and commercial banks to support Nigeria’s clean-energy infrastructure.

Parallel to financial reforms, Nigeria should leverage China’s new tariff-free African trade policy and regional AfCFTA rules to expand industrial production and export diversification. Under China’s current framework, countries such as Kenya, South Africa and Nigeria already benefit from duty-free access for selected products, opening China’s 1.4 billion-person market to Nigerian exports like palm oil, solid minerals and agro-processed goods. Indeed, it was noted that China’s new “tariff-free” African policy could let Nigeria export a wider range of goods (beyond oil) without import duties.

Yet the true opportunity lies in transforming raw exports into value-added, low-carbon products. By attracting Chinese investment in clean manufacturing technologies, for instance, solar-powered agro-processing, battery assembly, low-carbon cement production and green industrial parks, Nigeria can move up the value chain while aligning industrial growth with its ETP 2060. This transformation presents a win-win pathway:

Within the AfCFTA framework, Nigeria could also scale up production of higher-value goods such as processed cables, battery components and electric-vehicle parts for intra-African export. This dual strategy would help Nigeria achieve industrial scale while reinforcing China’s role as a partner in building green supply chains across Africa.

There is a need to scale up proven “small & beautiful” projects while preparing for GW-scale rollout, and it is also necessary to expand the catchment of peri-urban solar mini-grids and solar-home systems (SHS) with strong community contracts and anchor customers. Nigeria’s ETP envisions approximately 8.9 million mini-grid connections (104.8k mini-grids) and 5 million SHS by 2030.Chinese firms can deploy Direct Current-coupled (DC-coupled) solar-plus-storage microgrids in clusters of villages, and negotiate commercial-offtake (C&I) power purchase agreements with creditworthy local factories or Fast-Moving Consumer Goods (FMCG)/agro-processing plants. Utility-scale projects should also grow: Nigeria aims for about 200 GW of solar by midcentury, and Chinese EPCs could partner on multi-megawatt solar parks or gas/solar hybrids, given China’s strong gas-to-power and solar track record. In fact, the Federal Government has just signed a USD328.8-million contract with China’s CMEC to upgrade 330kV/132kV lines (544 km, 7,140 MW capacity), demonstrating China’s role in major transmission work. Importantly, these infrastructure plans should tie into the West Africa Power Pool (WAPP). WAPP is an ECOWAS initiative to integrate electricity markets (currently linking 13 of 14 member states) so that “areas of low generation” receive power from “areas of high supply,” promoting economies of scale. By aligning the new generation and grids with WAPP, Nigeria can export surplus power regionally.

Here, the need is to build out on-shore renewable-energy industries using Chinese capital and know-how.

Solar modules and inverters: encourage Chinese manufacturers to localize assembly (and eventually cell production). Recent deals show this is feasible: Redsolar (a China-Nigeria JV) signed for a 600 MW PV module factory in Kano State, and Oando Clean Energy has launched a 1.2 GW solar module assembly project (Africa’s first with a recycling line for old panels). Supporting such projects with land, incentives, and joint-venture financing will help build a solar supply base. Investment should also target after-sales services and quality-assurance hubs to address Nigeria’s warranty gap for off-grid kits.

Batteries and EVs: foster Chinese-Nigerian joint ventures to assemble battery packs (initially using imported cells) and establish recycling plants. China’s BYD, CATL and other battery leaders could share gigafactory and recycling expertise. At the same time, expand e-mobility assembly: Nigeria has already signed MoUs with Chinese partners to build electric tricycle (“e-trike”) assembly lines. Notably, top officials have urged China to help develop “full-cycle” EV manufacturing in Nigeria (from battery to vehicle). Chinese industry is responding. A recent announcement confirmed plans to build an EV plant in Nigeria, linking Nigerian lithium to EV battery production. Support for these ventures should include technical training, factory floor financing and integration with grid projects (e.g. solar-charging stations for vehicles).

Green hydrogen and fuels: use Nigeria’s abundant solar, wind and natural gas to produce green hydrogen and derivatives. Chinese electrolyzer firms can lead gigascale projects. For example, China’s LONGi (traditionally a PV maker) agreed a EUR7.6 billion preliminary deal to build a giant green-hydrogen-to-methanol complex in Nigeria (capable of 1.2 million tonnes/yr of green methanol). Similar projects could target green ammonia (for fertilizer or export) or compressed hydrogen. Nigeria should offer joint-venture land/loans for these ventures, potentially co-locating solar parks with electrolysis. Linking hydrogen to China’s supply chains (e.g. as fertilizer) would deepen clean-tech ties.

Critical minerals value chain: Nigeria should leverage its new policy barring raw ore exports by attracting Chinese investment in domestic refining and processing. Already, Chinese firms are deploying large lithium plants. A USD600-million lithium processing plant (Kaduna/Niger border) and a USD200-million refinery near Abuja are being commissioned this year with about 80% Chinese funding. Under Nigeria’s “local value-add” mining reforms, exporters must show plans for in-country refining. Sustained Chinese engagement here can turn Nigeria from a raw-miner exporter into a midstream supplier of battery-grade inputs (e.g. lithium salts, nickel cathodes). Similar opportunities exist in cobalt, manganese and other minerals critical for batteries and solar manufacturing.

Nigeria can build a transparent country platform blending Chinese and global climate finance. For instance, Nigeria could expand its new Climate Investment Platform (NCIP) into a multi-stakeholder “Green Industrial Development Platform.” The NCIP (launched in 2025) is designed to mobilize USD500 million by having the Nigeria Sovereign Investment Authority (NSIA) partner with the Green Climate Fund and local stakeholders. By co-creating this platform, Nigeria can string together Chinese concessional credit lines (e.g. for grid or renewable projects) with GCF grants, World Bank/IDA loans and domestic capital. As one GCF official noted, the goal is to “co-create a country platform that aligns with Nigeria’s climate strategy.” In practice, the Platform could match, say, a China-backed loan for a solar grid with an IDA grant for resilience training or a GCF grant for battery storage. Such integration ensures investments support Nigeria’s broader industrial policy (not just short-term sales). Nigeria should also pursue trilateral arrangements (China-Nigeria-multilateral coalitions) in forums like FOCAC and AfCFTA. For example, coordinated African Union’s New Partnership for Africa's Development (AU/NEPAD) initiatives on critical minerals and renewable tech-transfer (funded by mixed Chinese and Western sources) would formalize Africa-wide cooperation. Overall, by using its NCIP/NCSP frameworks, Nigeria can pool Chinese climate finance with Western climate funds and domestic investment in a transparent way, positioning the country as a hub for Sino–Western climate partnership.

In summary, Nigeria can leverage China‑Africa trade and investment ties across multiple fronts. Clear examples and references include China’s tariff‑waiver policy for Nigeria, the RMB-naira swap mechanism, large Chinese-backed power projects and recent Chinese‑Nigerian deals in solar, EVs and lithium processing. By knitting these opportunities into Nigeria’s own plans (ETP, AfCFTA, NCIP) and regional initiatives (WAPP, AU/NEPAD), the country can maximize jobs, industrial growth and climate gains from its China partnership.

Najim Animashaun is a non-resident fellow at the Africa Policy Research Institute (APRI), focusing on the political economy of energy. With over 30 years of experience as a legal and regulatory advisor, he has supported governments, development partners, and private sector actors in shaping energy policies across Africa.

Olumide Onitekun is APRI’s Research & Policy Officer for Climate Change, advancing Nigeria’s energy transition, methane mitigation in oil/gas, and integrating climate actions into national development plans.

Chibuikem Agbaegbu is a Climate & Energy Specialist with 12+ years in Sub-Saharan Africa. Expert in low-carbon electrification, energy nexus, climate transition & circular economy. Led donor/DFI projects with FCDO, USAID, EU, UNDP, GEF & more.