Can Nigeria’s mineral wealth power its own—and other countries'—energy transition? Explore how smart policies and investments can turn critical minerals into climate and economic opportunity.

Greenhouse gas (GHG) emissions from agriculture within the past 50 years have nearly doubled as a result of the increase in global food demand as well as changes in food consumption pattern (Ayayia, 2024). This sector's emissions primarily arise from activities related to crop production, livestock management and the use of synthetic fertilisers. Enteric fermentation in ruminant livestock (such as cattle, goats and sheep) is one of the largest sources of methane emissions in the agriculture sector. Methane is a potent GHG with a global warming potential many times greater than carbon dioxide (CO2).

The energy sector is responsible for a significant portion GHG emissions, primarily due to the extraction and use of fossil fuels. This sector contributes to emissions through energy-intensive production processes, often reliant on coal, oil, or gas.

As the world confronts the growing impacts of climate change, the global economy is shifting towards a low-carbon future, placing significant emphasis on clean energy technologies and sustainable development. This transition is driven by international commitments such as the Paris Agreement, which aims to limit global warming to well below 2°C, ideally to 1.5°C. To achieve this, countries are embracing renewable energy, electrification of transport and energy storage solutions.

Central to these technologies is the availability of certain minerals that are essential to produce a wide range of high-tech products, i.e. clean energy technologies, electronics and defence systems. The IEA has identified 50 minerals as "critical" for energy transition due to their economic importance, limited geographical availability and the potential risks associated with supply chain disruptions (IEA, 2023).

The importance of these minerals in ensuring the success of energy transition plans cannot be overstated. For example, lithium, cobalt and nickel are key components of lithium-ion batteries. These are the most widely used form of battery; powering electric vehicles, supporting grid-scale storage of energy generated from renewable sources and stabilizing decentralized energy systems. Rare earth elements (REE) such as neodymium and dysprosium are crucial for the production of high-efficiency magnets used in wind turbines and electric motors. Copper is essential for wiring solar panels, wind turbines and other renewable energy systems. Critical minerals are also used in the production of advanced materials that improve energy efficiency and in the development of sensors and tools for climate monitoring.

As countries accelerate their transition to low-carbon energy systems through the adoption of clean energy technologies on a larger scale, the demand for critical minerals is expected to rise exponentially. Between 2017 and 2022, the energy sector drove a threefold increase in overall demand for lithium, a 70 per cent increase in demand for cobalt and a 40 per cent rise in demand for nickel (IEA, 2023). By 2022, clean energy applications accounted for 56 per cent of total lithium demand, 40 per cent of total cobalt demand and 16 per cent of total nickel demand, up from 30 per cent, 17 per cent and six per cent, respectively, five years earlier (IEA, 2023). The IEA estimates that the demand for lithium could increase by over 40 times by 2040, while the demand for cobalt could increase by 20 to 25 times, driven largely by the rise of electric vehicles (EVs) and energy storage systems (IEA, 2021).

A few countries dominate the production of critical minerals, making the supply chains highly concentrated; for example, the Democratic Republic of Congo (DRC) supplies over 70 per cent of the world's cobalt, while China controls the majority of rare earth elements' refining capacity. This concentration poses risks of supply disruptions due to geopolitical conflicts, trade restrictions, or monopolistic control. Countries with significant reserves are leveraging their positions to strengthen their geopolitical influence, while major consumers are seeking to secure resilient and diversified supply chains to reduce dependence on dominant players like China. The United States (US), the European Union (EU) and other major economies have introduced policies to build strategic reserves, encourage domestic production and partner with resource-rich countries.

The extraction of critical minerals presents significant environmental and social risks. Mining activities often result in deforestation, water pollution, habitat destruction and the displacement of local communities. These environmental impacts can exacerbate climate change and undermine the benefits of clean energy technologies, leading to a paradox where the pursuit of climate goals comes at the expense of environmental sustainability.

For developing countries, the critical minerals boom offers a pathway to economic diversification, job creation and infrastructure development. In many cases, however, mineral-rich countries (particularly in Africa), have not fully benefited from their natural resources due to weak governance, corruption and exploitation by foreign companies. In addition, many mineral-rich countries have weak infrastructure and face ethical challenges, including child labour and unsafe working conditions in artisanal mines.

There are significant challenges in the development of a sustainable global critical minerals industry. There is a need to meet global demand for critical minerals while ensuring that extraction and processing adhere to sustainable and socially responsible practices. Initiatives that improve ethical sourcing and reduce the environmental impact of mining activities have been introduced by major economies. However, many countries need to adopt sustainable mining practices that mitigate negative environmental impacts while maximizing the economic benefits of mineral extraction. There is also the need to ensure that local communities benefit from mining activities, receiving a fair share of the revenues generated from mining and protecting their labor rights. Technological innovation, robust regulatory frameworks, strong governance structures, greater transparency and international cooperation to hold mining companies accountable for their environmental and social responsibilities are required to overcome these challenges.

The Nigerian economy whilst diverse, is heavily reliant on fossil fuels. Nigeria has set ambitious climate goals as part of its Nationally Determined Contributions (NDCs) under the Paris Agreement, pledging to reduce its greenhouse gas emissions by 20 per cent by 2030, with an additional 45 per cent reduction conditional on international support. Meeting these targets will require substantial investments in renewable energy, electrification and sustainable industrial practices.

In view of the phasing out of fossil fuel-based vehicles, the global shift to EVs and the growing demand for energy storage systems, Nigeria must rethink its energy strategy to balance its traditional reliance on oil and gas with the growing need to harness new opportunities presented by the global energy transition. Nigeria is endowed with a diverse range of mineral resources, including critical minerals. By leveraging its rich endowment of minerals, Nigeria could create a pathway toward meeting its own climate goals and emerge as a key supplier of these minerals thus driving economic growth. However, this will require the careful balancing of economic opportunities with environmental and social challenges, particularly regarding sustainable extraction, community engagement and value-added industries.

This research report aims to provide a comprehensive analysis of Nigeria's critical mineral landscape, identifying the key opportunities, challenges and policy recommendations for developing a sustainable critical minerals industry. The central question is: How can local policymakers drive the growth of Nigeria’s critical minerals sector to support the country's transition to a low-carbon economy, achieve its climate goals and drive its emergence as a key supplier of critical minerals?

This study employed a mixed-methods approach, combining desk-based research, stakeholder interviews and case study analysis to provide a comprehensive assessment of Nigeria's critical mineral landscape.

Nigeria’s transition to a low-carbon economy requires a strategic focus on sectors that contribute the most to the country's GHG emissions. The following sectors are key targets for decarbonization and critical minerals are essential for this transition:

The energy sector is responsible for a significant portion of Nigeria’s GHG emissions, primarily due to the extraction and use of fossil fuels. As shown in Figure 1, the energy sector produced the most emissions in 2021, producing 209 million metric tons of GHG emissions, constituting 62.4 per cent of total (Emission Index, 2024).

The sector's carbon intensity is driven by the reliance on oil and gas for electricity generation and industrial processes. Transitioning to renewable energy sources such as solar and wind is crucial. These technologies rely on critical minerals like silicon (for solar panels), rare earth elements (for wind turbines) and copper (for electrical wiring). By developing its own critical mineral resources, Nigeria can reduce its dependence on fossil fuels and lower its carbon emissions from the energy sector.

The transportation sector in Nigeria is also major emitter of GHGs, largely due to the widespread use of gasoline and diesel-powered vehicles. In 2021, transportation accounted for approximately 18 per cent of Nigeria’s total emissions, emitting 59 million metric tons of GHG (Emission Index, 2024). The adoption of EVs is key to decarbonizing the transportation sector. EVs require lithium, cobalt and nickel for their batteries. By investing in the extraction and processing of these minerals, Nigeria can support the domestic production and use of EVs, significantly reducing emissions from road transport.

In 2020, the sector constituted about 12.9 per cent of Nigeria’s direct CO2 emissions from the continuous utilisation of fossil-based energy and two per cent of electricity-related emissions (Emission Index, 2024).The manufacturing sector can be decarbonized through the adoption of energy-efficient technologies and the shift to renewable energy sources. Green hydrogen, produced using critical minerals like platinum and powered by renewable energy, is a potential solution for decarbonizing heavy industries such as steel and cement production.

Adoption of sustainable construction methods could also reduce the demand for heavy manufactured goods such as steel, cement, plastics. Such methods include increased use of recycled materials such as glass, newspaper, tyres etc; and extensive use of plant-based materials such as polyurethane rigid foam, mycelium, cob, laminated timber and bamboo.

The agriculture sector is a significant contributor to Nigeria's GHG emissions, accounting for approximately 24 per cent of the total in 2021 (Emission Index, 2024). Precision agriculture, which utilises technologies dependent on critical minerals like rare earth elements, can optimise fertiliser and water use, thereby reducing emissions. Additionally, the development of greener fertilisers, which require specific critical minerals, can help reduce the emissions associated with traditional synthetic fertilisers. Renewable energy technologies, powered by critical minerals, can also be used to electrify agricultural processes, reducing reliance on diesel-powered machinery.

According to Dr. Oladele Alake, Nigeria’s Minister of Solid Minerals Development, Nigeria’s valuable solid minerals deposits are estimated at over USD 700 billion (The Cable, 2023). Figure 2 is a map showing the NGSA’s depiction of the distribution of critical mineral deposits in Nigeria. Table 1 shows the location of the selected critical minerals in Nigeria. The NGSA claims to have a richer database of reserve information behind its paywall.

Nigeria’s copper deposits are estimated to be over 10 million tons, found in states like Zamfara and Bauchi (Foraminifera Market Research, 2015). Nigeria is also estimated to have the fifth largest lithium reserves in the world, with potential deposits located in the northeastern and north-central regions of the country (Ogunmola & Okunlola, 2020). Nigeria's cobalt resources are primarily found in the northeastern and north-central regions, with estimated reserves of around 700,000 metric tons. Other significant minerals include manganese, nickel, graphite, chromium, molybdenum, zinc, rare earths and silica sand, which are spread across different regions such as Plateau, Kaduna, Cross River, Katsina and Ebonyi. These minerals are strategically distributed across the country, offering diverse opportunities for mining and industrial development. However, the country's critical mineral resources remain underexplored and underdeveloped, with limited investment and infrastructure in place to support their exploitation and processing.

| S/N | Critical Mineral | Location |

|---|---|---|

| 1. | Copper | Zamfara, Bauchi, Kano, Yobe, Nasarawa, Plateau, Jigawa, Katsina |

| 2. | Lithium | Kogi, Nasarawa, Ekiti, Kwara, Cross River, Oyo, Plateau |

| 3. | Nickel | Kaduna, Osun, Katsina |

| 4. | Manganese | Niger, Edo, Adamawa, Kebbi, Borno, Cross River, Kaduna, Zamfara, Katsina |

| 5. | Cobalt | Adamawa, Kaduna, Katsina |

| 6. | Graphite | Kaduna, Adamawa, Niger, Bauchi; Cross River, Jigawa |

| 7. | Chromium | Zamfara, Katsina, Kaduna, Kogi |

| 8. | Molybdenum | Plateau, Ondo |

| 9. | Zinc | Cross River, Ebonyi, Benue, Nassarawa, Plateau, Taraba, Zamfara |

| 10. | Rare Earths | Ebonyi, Plateau |

| 11. | Silica Sand (Silicon) | Abia, Akwa Ibom, Anambra, Bayelsa, Benue, Bornu, Cross River, Delta, Enugu, Imo, Gombe, Jigawa, Kaduna, Kano, Katsina, Lagos, Nasarawa, Ondo, Niger, Ogun, Rivers, Sokoto, Taraba, Yobe, Zamfara |

Source: Aliu et al., 2022.

Nigeria's existing supply chain capabilities for critical minerals are limited, with the majority of the country's mineral resources being exported in raw or semi-processed form. The country lacks the necessary processing facilities, technical expertise and infrastructure to fully capitalise on its critical mineral endowment. In 2022, the Nigerian government set up six processing plants across the six geopolitical zones (Bauchi, Oyo, Kano, Ebonyi, Cross River, Kogi) intended to boost the domestic processing capabilities of critical minerals (NIPC, 2022).

Leveraging funding from the COVID 19 Intervention Fund of the Central Bank, the government has established six mining hubs in each of the geopolitical zones of Nigeria:

Each of these, the government hopes will advance its goals of driving processing, export led growth, value addition, training of local workforce and ultimately building ecosystems which catalyse private sector investment around the hubs. However, stakeholders interviewed report that these plants are not yet fully functional and the status of their operationalization is low at best. This delay hampers the development of a local supply chain and forces reliance on the export of raw materials.

The development of critical minerals in Nigeria is contingent on the existence of a robust enabling environment. This environment encompasses the legal and regulatory framework, institutional capacity, infrastructure, availability of financing and political stability, all of which play a pivotal role in attracting investment, fostering sustainable development and ensuring that Nigeria can effectively harness its critical mineral resources.

Nigeria’s legal and regulatory framework for mining is governed primarily by the Nigerian Minerals and Mining Act of 2007, the Nigerian Minerals and Mining Regulations, 2011 and the National Minerals and Metals Policy. These laws serve as the primary legislation regulating mining activities in Nigeria, providing the basis for mineral exploration, extraction and investment, for the issuance of mining licenses and leases and outlining the rights and obligations of mining operators. However, the existing legal framework lacks specific provisions for the exploitation of critical minerals.

Key institutions such as the MMSD and the NGSA are responsible for overseeing the critical minerals sector. However, these institutions often face challenges related to funding, skilled manpower and operational inefficiencies, which hinder their ability to effectively regulate and support the industry.

The Nigerian Mining Cadastre Office (NMCO) is responsible for processing applications for mineral titles and permits and application for the transfer, renewal, modification and relinquishment of mineral titles or extension of areas. Their processes are well documented on their website. As part of its commitment to revitalising the solid minerals sector, the Nigerian government has embarked on a comprehensive cleanup of the licensing regime. This effort is aimed at ensuring that licences are held by entities with the genuine capacity and intent to explore and develop critical mineral resources. The government has revoked 2,531 dormant licences and awarded 499 new licences, including 146 lithium mining licenses (Business Post, 2024).

The Nigerian government has implemented numerous initiatives aimed at developing the critical minerals sector, yet several challenges have hindered the full realisation of these initiatives.

Nigeria's critical minerals sector is deeply intertwined with the country's political economy, where governance, economic interests and power dynamics play crucial roles. However, the sector offers significant opportunities.

Nigeria's critical mineral resources have the potential to serve both domestic and international markets. Key potential export markets include China, the US and the EU, all of which are actively seeking to diversify their critical mineral supply chains. The global lithium market was valued at approximately USD 37.8 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 22.1per cent from 2023 to 2030, reaching USD 89.9 billion by 2030 (Global News Wire, 2023). The global cobalt market was valued at around USD 15.9 billion in 2022, with strong growth prospects due to the rising demand for EV batteries (Grandview Research, 2023). Lithium carbonate prices have also surged due to supply constraints and increasing demand, with prices exceeding USD 20,000 per tonne in recent months (Carbon Credits, 2024). Given the current high prices of lithium carbonate, Nigeria stands to generate significant revenue from exports. For instance, exporting 100,000 tonnes (circa 14 percent of global supply) annually at current prices could yield over USD 2 billion.

Nigeria could attract foreign direct investments (FDI) from major manufacturers of green technologies. Companies from countries leading in battery manufacturing, such as China, South Korea and Japan, are particularly interested in securing a steady supply of lithium. Forming partnerships with global clean technology giants could provide technological and financial support, ensuring sustainable extraction and processing practices.

The development of a critical minerals industry could support the country's growing clean energy sector, including the manufacture of solar panels, wind turbines and electric vehicles. Beyond exporting raw materials, Nigeria has the opportunity to develop a domestic battery manufacturing industry and manufacturing of other green technologies. As demonstrated in the Australian illustration below, there is more value downstream than in simply exporting raw material. Establishing research and development centres focused on battery technology and sustainable mining practices could position Nigeria as a leader in the African clean energy sector.

With adequate investments in processing plants, Nigeria could become a regional hub for lithium processing, importing lithium ore from other African countries and processing it for export. This could enhance Nigeria's strategic importance in the global supply chain for critical minerals.

Regional cooperation in the critical minerals industry

The African Union’s African Mining Vision (AMV) provides a framework for sustainable mineral development on the continent, emphasizing good governance, local beneficiation and regional cooperation. By strengthening resource governance and promoting value addition, Nigeria and other African countries can ensure that critical minerals contribute to sustainable development and economic diversification. Regional cooperation can also help African countries pool resources, build infrastructure, negotiate better terms in global supply chains. This will strengthen their position, ensure that the economic benefits of mineral wealth are maximized and reduce vulnerability to the boom-and-bust cycles of raw commodity exports, providing a more stable foundation for long-term growth.

Nigeria's critical mineral resources present an opportunity for the country to enhance its geopolitical influence, similar to the role it has played in the Organization of the Petroleum Exporting Countries (OPEC) with its oil and gas resources. Key players in Nigeria's critical minerals space include China, the EU, the US and other emerging markets such as India and Russia. These actors have increasingly recognized Nigeria's potential as a significant source of critical minerals required for green technologies.

China’s strategy is often driven by securing long-term supply chains for its manufacturing sector; its involvement in Nigeria's critical minerals sector is significant, marked by substantial investments in infrastructure and mineral exploration. Chinese companies, such as Huayou Cobalt, have been actively pursuing opportunities in Nigeria. While China’s investment is vital, over-dependence could expose Nigeria to vulnerabilities, including geopolitical leverage by China. Nigerian sub-nationals must be mindful of agreements they sign that may contain contingent liabilities that leave future Nigerians in debt, including judgement debts such as was the case with the Guangdong Free Trade Zone (OGFTZ), where a judgement has put Nigeria in debt to the tune of USD 70 million in exchange for a perimeter fence built by the Chinese.2

European companies like Anglo American (UK) and Glencore (Switzerland) are also key players in Nigeria. The EU's approach is shaped by its Green Deal and the need for sustainable sourcing of critical minerals. European investments in Nigeria are often tied to ensuring ethical and environmentally responsible mining practices, aligning with the EU's stringent regulatory standards. These stringent environmental and social requirements that might be challenging to meet in the short term but may be beneficial in the long run.

By strategically positioning itself as a reliable supplier, Nigeria could negotiate more favourable trade agreements, attract foreign investment and play a pivotal role in shaping global energy transition policies. This influence could also allow Nigeria to participate in international alliances and negotiations, potentially giving it a stronger voice on the global stage, particularly in matters related to sustainable development, climate change and resource management. As Nigeria navigates its relationships with these global powers, a balanced approach will be crucial. The global scramble for critical minerals could also expose Nigeria to geopolitical tensions, particularly if it becomes a battleground for influence between China and Western powers. Nigeria must carefully navigate these waters to avoid being caught in a new form of resource-driven Cold War, where its resources are exploited at the expense of long-term national interests.

This study examined the critical minerals strategies countries that have made significant progress in developing their critical minerals industries. These case studies provide valuable insights that could inform Nigeria's approach to critical minerals development.

Australia has identified critical minerals as a key priority for economic development and has implemented a comprehensive policy framework to support the industry. The country has invested heavily in geological mapping, exploration and research to better understand its critical mineral resources. Australia has also focused on attracting foreign direct investment, fostering public-private partnerships and developing a skilled workforce to support the critical minerals industry.

Australia currently produces 335,000 tonnes of lithium carbonate equivalent (LCE) and is expected to increase up to 470,000 by 2024 (Figure 3). This is projected to provide over 52 per cent of the world’s lithium demand of 1.5 million tonnes of LCE by 2024 (World Economic Forum. 2023). In 2017, Australia identified that the least value obtained was in the mining stage and the most value obtained is in the battery pack system assembly stage (Figure 4). Australia earned less than one per cent of the ultimate value of lithium-ion battery packs. Approximately, 99.5 per cent of the value of lithium is added through offshore processing, cell production and battery assembly. The country therefore set a goal to increase its participation in the downstream processing of its lithium and set out to reduce its dependence on Asian countries in this regard.

The US has designated critical minerals as essential for national security and economic prosperity and has developed a whole-of-government strategy to ensure a reliable supply. The strategy includes measures to increase domestic production, improve recycling and reuse and strengthen international partnerships to diversify supply chains. The US has also invested in research and development to support technological innovations in critical minerals processing and manufacturing.

The strategy focuses on six pillars:

The US Government has invested USD 3.5 billion from the Infrastructure Law to boost domestic production of advanced batteries and battery materials (Energy.gov, 2023). In addition, through its Loan Programs Office, the US has invested USD 59 billion so far in domestic loans to energy projects and is expected to invest another USD 150 billion in a few years (Energy.gov, 2023).

The DRC and Morocco are emerging as leaders in battery manufacturing in Africa. The DRC has abundant reserves of critical raw materials (CRMs) needed for battery production, such as cobalt, lithium, copper and graphite. It holds over 50 per cent of the world's cobalt reserves (AfDB, 2023), a key component in lithium-ion batteries and in 2020 produced about 70 per cent of the global cobalt supply. The government has partnered with the UN Economic Commission for Africa, Afreximbank and other entities to identify ways to increase the DRC's share of the battery and electric vehicle value chain.

A 2021 feasibility study commissioned by the World Bank and Bloomberg NEF confirmed that setting up a 10,000 tonnes battery precursor3 manufacturing facility in the DRC would be technically feasible and financially viable, with an estimated total cost of USD 39 million (Bloomberg, 2021). This is three times cheaper than what it would cost for a similar plant in the U.S. A similar project in China and Poland will cost USD 112 million and USD 65 million, respectively. The DRC's proximity to raw materials and access to cheap hydroelectric power from the Congo River provide significant cost advantages compared to battery production in places like the US or Poland.

In May 2023, Chinese battery manufacturer GOTION HIGH-TECH signed a USD 6.4 billion agreement with the Moroccan government to set up battery and energy storage production facilities with an annual capacity of 100 GWh. This investment is expected to create 25,000 jobs over the next 10 years and position Morocco as a strategic hub for battery production, leveraging the country's mineral wealth and automotive manufacturing expertise.

Morocco is already an automotive manufacturing hub for global automakers like Stellantis and Renault, giving it a strong industrial base to build upon. The country's political stability, business-friendly policies and access to renewable energy sources like solar and wind power make it an attractive destination for battery investments (Karkanare & Medinila, 2023).

By leveraging their natural resource endowments and strategic partnerships, these countries are positioning themselves to capture a share of the rapidly growing global battery and electric vehicle market. Continued investment in supply chain infrastructure, skills development and an enabling policy environment will be crucial to realising their full potential. Morocco's success in attracting significant investment in battery manufacturing is partly due to its existing automotive industry.

For Nigeria’s energy security and national income objectives, developing the refining industry for critical minerals is the current priority. However, developing national strategies to advance to the value-adding stages of electrochemical production and battery assembly are required to serve the demands of the power sector in Africa.

The DRC's collaboration with international entities like the UN Economic Commission for Africa and Afreximbank to explore its role in the battery and EV value chain is a critical step towards enhancing its global standing. Nigeria can adopt a similar strategy by engaging with global financial institutions and organizations to access funding, technical expertise and markets for its critical minerals sector.

By strengthening its industrial base, as in the case of Morrocco, particularly in sectors aligned with critical minerals, Nigeria can attract similar large-scale investments in its industry.

Although Nigeria has reserves of over 40 solid minerals, including recent high-grade lithium discoveries, the sector has historically struggled to attract the necessary investment due to the capital-intensive nature of mining. To address these challenges, Nigeria has implemented a series of financing initiatives to support junior mining companies and artisanal miners, creating a more favourable environment for both local and foreign investments.

One of the key initiatives is the partnership between the Africa Finance Corporation (AFC) and the Solid Minerals Development Fund (SMDF), which aims to de-risk mining projects and scale artisanal mining operations to an industrial level. This partnership aims to catalyse the growth of the mining sector by providing necessary funding and technical support worth USD 700 million to advance projects from exploration to full feasibility, construction and operation. This initiative aims to increase the pipeline of investment-ready projects, thus attracting more capital into the sector.

The Bank of Industry (BOI) has also introduced an intervention fund that provides loans to artisanal miners on favorable terms, allowing them to formalize their operations and scale up sustainably. Another significant initiative is the Nigerian Artisanal and Small-Scale Miners Financing Support Fund: a NGN 5 billion (USD 3.2 million) facility that offers financing ranging from NGN 100,000 to NGN 100 million (USD 65 to USD 64,685), depending on the scale of the miner’s operations.

Private sector activity, particularly from Chinese investors, has also ramped up in Nigeria’s critical minerals sector. Avatar New Energy Materials, a Chinese company, invested USD 100 million to establish Nigeria's largest lithium processing plant in Nasarawa State, with a capacity of 4,000 tonnes per day (Business Day, 2024). Canmax Technologies, responsible for over 30 per cent of global battery material production, is investing USD 200 million in another lithium plant in the same region (Statehouse, 2024). ASBA Group is constructing a USD 50 million Lithium Ore Separation Plant and 6 MW CNG Gas Power Plant in Abuja, expected to generate USD 350 million annually (Advisor Reports, 2024). Additionally, global miner Glencore has shown interest in entering Nigeria’s critical minerals sector (Reuters, 2024). These projects align with Nigeria’s policy to ensure domestic processing of critical minerals before export, reflecting the government's goal of promoting local value addition and maximizing the economic benefits from these resources.

Nigeria's commitment to developing an integrated value chain for critical minerals was demonstrated in 2022 when the government turned down an offer from Elon Musk’s Tesla to mine lithium in Nigeria. Tesla’s inability to commit to establishing a battery manufacturing facility in the country led to the rejection of its proposal, highlighting Nigeria’s firm stance on ensuring that companies contribute to local processing and value creation.

International partnerships have further enhanced Nigeria’s capacity in the mining sector. The Nigeria-U.S. mining partnership aims to bolster technical expertise, particularly in critical minerals like lithium, while providing regulatory support to attract foreign investments. Similarly, Nigeria’s collaboration with the World Bank has focused on governance reforms and capacity building in the mining sector, which has helped improve the regulatory environment and investment landscape for critical minerals.

These concerted efforts by the Nigerian government, supported by international partnerships and increasing private sector investments, are positioning Nigeria as a key player in the global clean energy transition. While challenges such as regulatory uncertainties, infrastructure deficits and security concerns remain, Nigeria's vast mineral wealth and ongoing reforms offer significant opportunities for growth in the critical minerals market.

There is potential across the critical minerals value chain in Nigeria, from exploration and mining, to processing and refining, to manufacturing green technologies. Then there are the soft sciences of distribution and exports, recycling and research and innovation. We explore the opportunities at each step next.

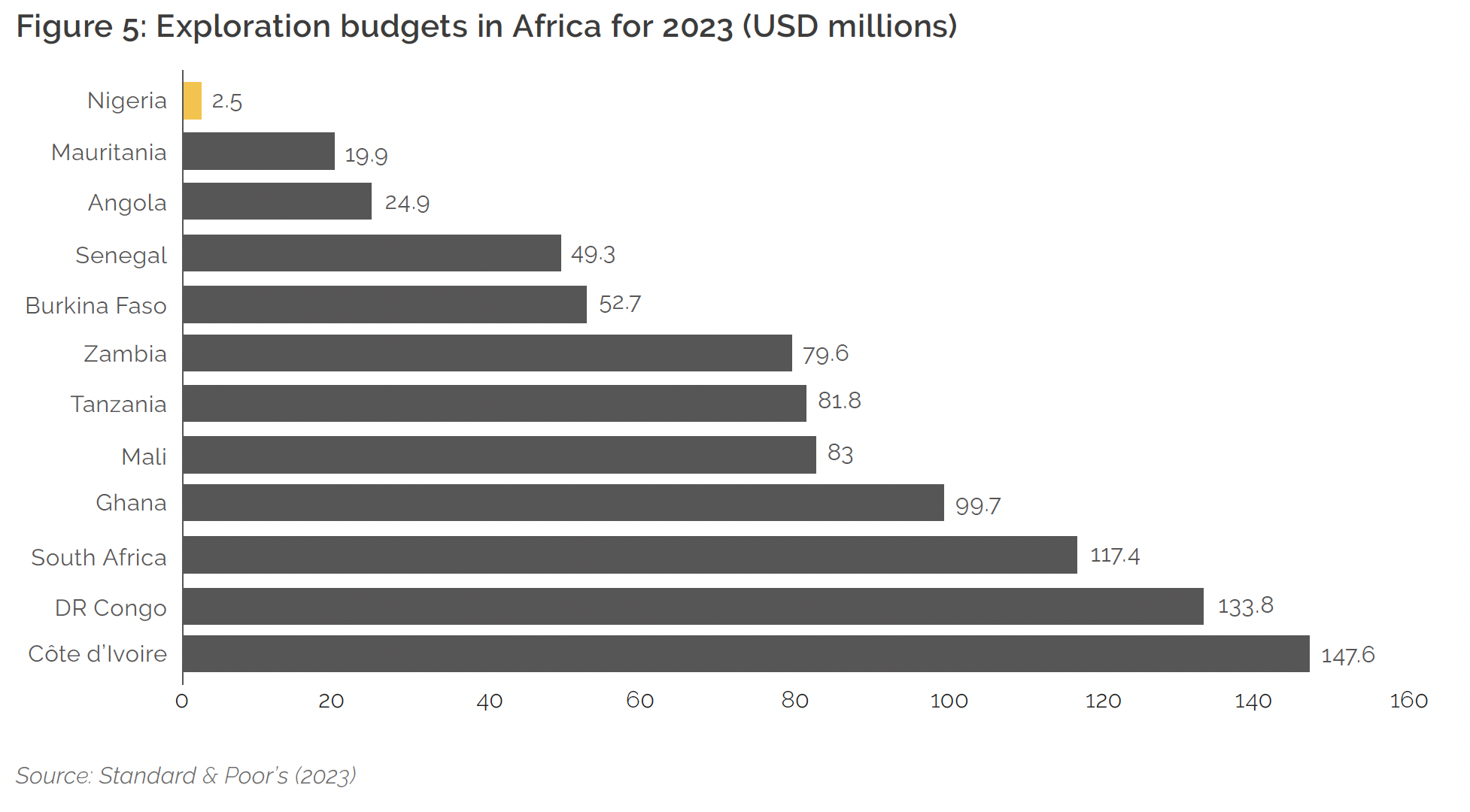

Nigeria's exploration activities remain underfunded, with annual spending estimated around USD 2.5 million, significantly lower than regional peers like Côte d'Ivoire (USD 147 million) and Congo (USD 133 million) (Standard & Poor’s, 2023). Current underinvestment hampers the ability to accurately assess mineral reserves, thereby limiting strategic planning and investment attraction.

To bridge this gap, from peer benchmarking, an annual investment of between USD 74.4 million and USD 100 million is necessary to conduct comprehensive geological surveys and exploratory drilling across the country’s vast untapped potential, with USD 74.4 million being the average exploration budget of the groups of countries shown in Figure 5.

The current state of processing infrastructure in Nigeria is severely lacking; there are few facilities available for refining critical minerals and most minerals exported in raw or semi-processed form. However, recent investments in Nigeria's critical minerals processing sector highlight increasing global interest and the potential to retain more value domestically. Establishing the necessary processing plants is essential, with each large-scale facility (e.g., for lithium or cobalt) costing between USD 100 million to USD 500 million (Energy Capital, 2024). Given the need for at least three to four major plants to meet both domestic and export demands, the country requires approximately USD 500 million per facility. This investment would enable Nigeria to maximize the economic benefits of its mineral resources, create thousands of jobs and stimulate local economies, further solidifying Nigeria's role in the global supply chain.

The downstream manufacturing sector, such as battery production, is another area where Nigeria faces significant funding gaps. The global battery market alone is projected to reach USD 400 billion by 2030. Establishing local production facilities could allow Nigeria to capture a significant share of this market, reducing the need for imports and fostering a local green technology industry. Additionally, producing EV components could integrate Nigeria into the global automotive supply chain, attracting further investment from global automakers. Establishing a battery manufacturing plant, for instance, typically requires investments ranging from USD 100 million to USD 1 billion, depending on the scale. An estimated USD 1 billion over five years is needed to build and scale these manufacturing capabilities, positioning Nigeria as a competitive player in the global supply chain for critical minerals.

With a developed supply chain, Nigeria could become a leading exporter of refined critical minerals and green technology components. Inadequate transportation infrastructure, particularly in remote mining regions, presents a substantial bottleneck for the sector. Strategic trade agreements and infrastructure improvements, such as upgrading ports and railways, would be essential to facilitate this. The cost of upgrading these infrastructures —roads, railways and ports — can range from hundreds of millions to over a billion dollars, depending on the extent of development required. An investment of between USD 100 to 150 billion per annum (Andersen Nigeria, 2024) for the next ten years is required to bridge Nigeria’s infrastructure gap, which is necessary to ensure efficient transport of minerals from extraction sites to processing facilities and export hubs. This investment is critical for making Nigeria’s critical minerals accessible to global markets and increasing the competitiveness of its supply chain.

To ensure sustainability, Nigeria should invest in recycling facilities for critical minerals. Recycling lithium, cobalt and nickel from used batteries could reduce the environmental impact of mining and provide a secondary supply of these valuable materials. By 2032, the recycling market for lithium-ion batteries is expected to grow to USD 24 billion (Statista, 2024). Developing this capability would support a circular economy, reduce waste and enhance Nigeria's sustainability credentials.

There is a significant gap in research and development (R&D) investment in Nigeria's critical minerals sector. To build local expertise and reduce dependency on foreign technologies, Nigeria needs to allocate approximately USD 50 million annually to R&D. This would support the adoption of advanced geoscience technologies for exploration, the development of new processing methods and the promotion of sustainable mining practices. It would also help the country stay ahead in a rapidly evolving global market, ensuring that Nigeria can compete effectively on the basis of innovation and efficiency.

Based on the findings of this research, the following recommendations are proposed to support the development of a sustainable critical minerals industry in Nigeria:

Nigeria's abundant critical mineral resources present a significant opportunity for the country to support its energy transition and drive sustainable economic growth. The demand for critical minerals, driven by the global transition to a low-carbon economy, presents Nigeria with the chance to become a key player in the supply of essential materials for clean energy technologies.

However, realizing this potential requires addressing significant challenges. The current state of Nigeria's critical minerals sector is hampered by inadequate exploration investment, limited processing capabilities and a complex regulatory environment. The ongoing issues with the legislative framework, underdeveloped infrastructure and lack of comprehensive geological data further exacerbate these challenges.

The Nigerian government has demonstrated a commitment to overcoming these obstacles through initiatives such as the National Single Window and the establishment of lithium processing plants. Yet, these efforts must be supported by a cohesive and strategic approach to critical minerals development.

To fully capitalize on its mineral resources, Nigeria must develop a comprehensive critical minerals strategy, strengthen regulatory and governance frameworks, invest in geological mapping and exploration and build robust processing and refining capabilities. Additionally, fostering collaboration with international partners, investing in skills development and promoting sustainable mining practices are crucial steps.

Addressing these issues and implementing the recommended strategies will not only enhance Nigeria's position in the global critical minerals market but also contribute significantly to the country's economic diversification and sustainable development. By leveraging its mineral wealth, Nigeria can position itself as a key player in the global clean energy supply chain.

The implementation of the recommendations outlined in this report will require a coordinated and sustained effort from the Nigerian government, industry and other stakeholders. However, the potential benefits of a thriving critical minerals industry, in terms of job creation, economic diversification and environmental sustainability, make this a worthwhile endeavour for the country.

Advisors Reports. (2024, July 31). Nigeria’s second lithium factory takes off in Abuja with $50M investment, featuring 6MW CNG gas power plant. https://advisorsreports.com/nigerias-second-lithium-factory-takes-off-in-abuja-with-50m-investment-featuring-6mw-cng-gas-power-plant/

African Development Bank. (2023). Rich in green minerals, African countries eye booming electric vehicle and clean energy market worth trillions of dollars. https://www.afdb.org/en/news-and-events/rich-green-minerals-african-countries-eye-booming-electric-vehicle-and-clean-energy-market-worth-trillions-dollars-65241

Alake, D. (2023, September). Nigeria's solid minerals sector valued at over $700bn. The Cable. Retrieved fromhttps://www.thecable.ng/dele-alake-nigerias-solid-minerals-sector-valued-at-over-700bn/

Aliu, H., Saheed, R., Aliu, I., & Qasim, K. (2022). The availability of critical minerals for Nigeria's renewable energy and economic development: An assessment of the role of nanotechnology. Nano Plus: Sci. Technol. Nanomat. 5 (2022) 1-109

Andersen Nigeria. (2024, August 2). Bridging Nigeria’s infrastructure deficit through Infracorp: Prospect, challenges and future outlook https://ng.andersen.com/bridging-nigerias-infrastructure-deficit-through-infracorp-prospect-challenges-and-future-outlook/

Ayayia, G. S. (2024). Policy Pathways for Greenhouse Gas Emissions: A Sector-Specific Approach in Nigeria's Agriculture, Forestry and Energy. Retrieved from

Bloomberg NEF. (2023). The cost of producing battery precursors in the DRC. https://assets.bbhub.io/professional/sites/24/BNEF-The-Cost-of-Producing-Battery-Precursors-in-the-DRC_FINAL.pdf

BusinessDay. (2024, July 31). Tinubu welcomes Nigeria’s largest lithium plant. https://businessday.ng/news/article/tinubu-welcomes-nigerias-largest-lithium-plant/

Business Post Nigeria. (2024, July 29). Nigeria approves 146 lithium mining licenses. https://businesspost.ng/economy/nigeria-approves-146-lithium-mining-licenses/

Carbon Credits. (2023). Lithium priced at over $20,000 per ton signals market optimism. https://carboncredits.com/lithium-priced-at-over-20000-per-ton-signals-market-optimism/

Daily Post Nigeria. (2024, May 23). FG prohibits companies from processing Nigeria’s resources abroad. https://dailypost.ng/2024/05/23/fg-prohibits-companies-from-processing-nigerias-resources-abroad

Emissions Index. (2024). Greenhouse Gas Emissions in Nigeria

Energy Capital & Power. (2024, August 1). Top 10 lithium mines in Africa. https://energycapitalpower.com/top-10-lithium-mines-in-africa/

European Centre for Development Policy Management. (2023, June 5). African battery value chain: Kickstart green industrialisation. https://ecdpm.org/work/african-battery-value-chain-kickstart-green-industrialisation

Foraminifera Market Research. (2015). Copper ore mining Nigeria: The pre-feasibility report. Retrieved from https://foramfera.com/marketresearchreports/mining-and-quarrying/copper-ore-mining-in-nigeria-the-pre-feasibility-report/

GlobeNewswire. (2023, June 20). Lithium market to grow USD 89.9 billion by 2030 with a 22.1percent CAGR. https://www.globenewswire.com/en/news-release/2023/06/20/2690748/0/en/Lithium-Market-to-Grow-USD-89-9-Billion-by-2030-With-a-22-1-CAGR.html

Grand View Research. (2023). Cobalt market report. https://www.grandviewresearch.com/industry-analysis/cobalt-market-report#:~:text=Thepercent20globalpercent20cobaltpercent20marketpercent20size,cobaltpercent20duringpercent20thepercent20forecastpercent20period.

International Energy Agency. (2023). Critical Minerals Market Review 2023. IEA. https://www.iea.org/reports/critical-minerals-market-review-2023

International Energy Agency. (2021). The Role of Critical Minerals in Clean Energy Transitions.https://www.iea.org/reports/critical-minerals-market-review-2023/key-market-trends#abstract

McKinsey & Company. (2021, December 14). Battery 2030: Resilient, sustainable and circular. https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/battery-2030-resilient-sustainable-and-circular

Nigerian Investment Promotion Commission. (2022, February 19). FG to build 6 solid minerals processing plants. https://www.nipc.gov.ng/2022/02/19/fg-to-build-6-solid-minerals-processing-plants/

Nigeria Ministry of Power. (2023). Power sector presentation at AEF 2023. Africa Energy Forum. https://cdn.asp.events/CLIENT_EnergyNe_9A2AD9E1_052D_C466_21FA5F6F01D93263/sites/AEF-2022/media/libraries/new-pres-library/D2---09.45---CS---NIGERIA_PS-Presentation-at-AEF-2023-SEMI-FINAL.pdf

Ogunmola, J. K., & Okunlola, O. A. (2020). Lithium Potential in Nigeria: A Review. Journal of Geoscience and Environment Protection, 8(4), 1-12.

Okunlola, O. A., & Ogunmola, J. K. (2019). Cobalt Mineralization in Nigeria: Occurrence, Exploration and Potential. Journal of Geoscience and Environment Protection, 7(3), 1-12.

Reuters. (2024, April 26). Glencore seeks investment opportunities in Nigerian mining sector. https://www.reuters.com/markets/commodities/glencore-seeks-investment-opportunities-nigerian-mining-sector-2024-04-26/

State House Nigeria. (2024, July 30). My government is set to make Nigeria the solar panel and EV battery manufacturing hub of Africa—President Tinubu. https://statehouse.gov.ng/news/my-government-is-set-to-make-nigeria-the-solar-panel-and-ev-battery-manufacturing-hub-of-africa-president-tinubu/

Statista. (2023). Global market value of lithium-ion battery recycling from 2021 to 2030. Statista. https://www.statista.com/statistics/1330758/lithium-ion-battery-recycling-market-value-worldwide/

This Day Live. (2024, May 11).Tinubu inaugurates lithium processing factory in Nasarawa.

U.S. Department of Energy. (2023, February 15). Biden-Harris administration announces $3.5 billion to strengthen domestic battery manufacturing.

U.S. Department of Energy. (n.d.). Portfolio projects. https://www.energy.gov/lpo/portfolio-projects

Vanguard. (2024, May 17). Solid minerals dev’t: Alake laments Nigeria’s 12th position in exploration budget. https://www.vanguardngr.com/2024/05/solid-minerals-devt-alake-laments-nigerias-12th-position-in-exploration-budget/

World Bank. (n.d.). Economy profile of Nigeria. Doing Business. https://archive.doingbusiness.org/en/data/exploreeconomies/nigeria

World Economic Forum. (2023). The countries that produce the most lithium in the world.

[1] Marshallian externalities refer to the concept of increasing returns to scale in an industry, where the production of one firm benefits other firms in the same industry.

[2] As reported by FIJ. Retrieved from https://fij.ng/article/chinese-firm-that-seized-nigerias-presidential-jets-was-months-old-when-it-got-ogun-contract/

[3] Precursor refers to the mining and electrochemical phases of battery production. The feedstocks used in the production of lithium-ion batteries are in the form of metal salts, predominantly sulfates. The sulfates for cobalt, nickel and manganese are combined in various ratios depending on the chemistry type to form the precursor cathode active material (precursors). The precursors are then combined with either lithium carbonate or lithium hydroxide, depending on battery chemistry, to form the cathode active material. The cathode active materials are then combined with the anode material, predominantly graphite, to form the battery cells. The cells are finally assembled into a battery pack, which then goes into an electric vehicle

Dr. (Engr.) Tobi Oluwatola is Founder/ CEO of TAO Pan African Energy, a renewable energy technology company building minigrids and developing software for energy services in West Africa and the North America. Dr Oluwatola is also a Senior Renewable Energy Advisor for the United Kingdom Nigeria Infrastructure Advisory Facility (UKNIAF).